Invoicing Non-EU Customers from Germany 2026: Third-Country Invoice Rules for GmbH and Freelancers

How GmbH owners, UGs and freelancers in Germany invoice customers outside the EU, mandatory fields, the right VAT note, foreign currency, and the correct UStVA line.

- Category

- Invoicing

- Updated

- Author

- Diana Chebotareva

US agencies, UK enterprises, Swiss family businesses, Australian startups, if you run a GmbH, UG or freelance business in Germany with customers outside the EU, you need to issue a third-country invoice. The rules differ from German or EU invoicing, and the wrong note either costs you input VAT or triggers questions from the tax office. Here's how to do it right, from the VAT note to the correct line in your VAT return.

The essentials at a glance

- Third country means any country outside the EU: the US, UK, Switzerland, Norway, Australia and every other non-EU state.

- B2B service: the place of supply is at the customer (§ 3a Abs. 2 UStG), the service is not subject to German VAT, so no VAT line on the invoice.

- Goods export: VAT-exempt under § 6 UStG, but only with export proof (the exit certificate from the ATLAS procedure).

- Required note: for services "Not subject to German VAT", for goods exports "VAT-exempt export under § 6 UStG".

- No EC Sales List and no OSS for third countries, both only apply inside the EU.

- VAT return: goods exports go in line 24 (code 43), non-taxable B2B services in line 41 (code 45), many people mix these up.

- Foreign currency is converted to euros at the official monthly BMF rate (§ 16 Abs. 6 UStG).

What is a third-country invoice?

A third-country invoice is an invoice to a customer based outside the European Union, the US, UK, Switzerland, Norway, Australia, or any other non-EU state. The rules for VAT and the required fields differ from invoices inside Germany or the EU. For SaaS providers, agencies, consultants and IT freelancers in Germany, this is daily business.

Note: "third country" is a VAT term, not a geographic one. Switzerland sits in the middle of Europe but isn't an EU member, so it's a third country; the specifics of invoicing there are covered in the VAT on invoices to Switzerland guide. The UK has been a third country since Brexit. Northern Ireland has a special status for goods and still counts as EU territory there.

Third country, EU or domestic: the key difference

Inside the EU, you either apply reverse charge or document an intra-community supply, both require a valid EU VAT ID from the customer and must be reported in the EC Sales List. In a third country there is no EU VAT ID, and you don't file an EC Sales List either. Instead, most B2B services are simply not subject to German VAT (§ 3a Abs. 2 UStG for services, § 6 UStG for goods exports).

| Customer | VAT on the invoice | Requirement | Reporting |

|---|---|---|---|

| Germany (B2B/B2C) | yes, 19% or 7% | – | VAT return |

| EU B2B | no (reverse charge) | valid EU VAT ID | VAT return + EC Sales List |

| EU B2C | yes, possibly via OSS | – | VAT return / OSS |

| Third-country B2B (service) | no, not taxable | customer is a business | VAT return (line 41) |

| Third country (goods export) | no, exempt § 6 UStG | export proof | VAT return (line 24) |

| Third-country B2C (digital) | possibly local tax in the customer's country | – | local in the customer's country |

When German VAT does not apply

In most cases you charge no German VAT on a third-country invoice, but for two different legal reasons that you must not confuse:

- B2B services to a third country: the place of supply shifts to the customer's country (§ 3a Abs. 2 UStG). The service is not subject to German VAT, it doesn't appear as a taxable transaction in the German VAT system at all. This covers consulting, IT, software development, marketing, design and similar services to non-EU businesses.

- Goods exports: the supply is VAT-exempt under § 4 No. 1a in conjunction with § 6 UStG, it would be taxable in principle but is exempt as long as you provide export proof.

- B2C services: special rules apply, especially for electronically supplied services (see below).

The practical difference: "not taxable" (service) and "exempt" (goods export) go to different lines in the VAT return and need different notes on the invoice.

The right VAT note on the invoice

A third-country invoice without a VAT note is incomplete. Which sentence belongs on it depends on the transaction:

| Case | Note on the invoice |

|---|---|

| B2B service to a third country | "Not subject to German VAT (§ 3a Abs. 2 UStG)" |

| Goods export to a third country | "VAT-exempt export under § 6 UStG" |

| Third country with its own reverse-charge system (e.g. Switzerland, UK) | additionally "Reverse charge" |

For international clients the note usually goes on the invoice in English, a third-country customer can't do much with "§ 3a Abs. 2 UStG", but "Not subject to German VAT, reverse charge" makes sense to them. Whether the customer has to account for a tax in their own country (such as Swiss acquisition tax or US sales/use tax) is governed by their local law, that's not your job, but a clean note helps them.

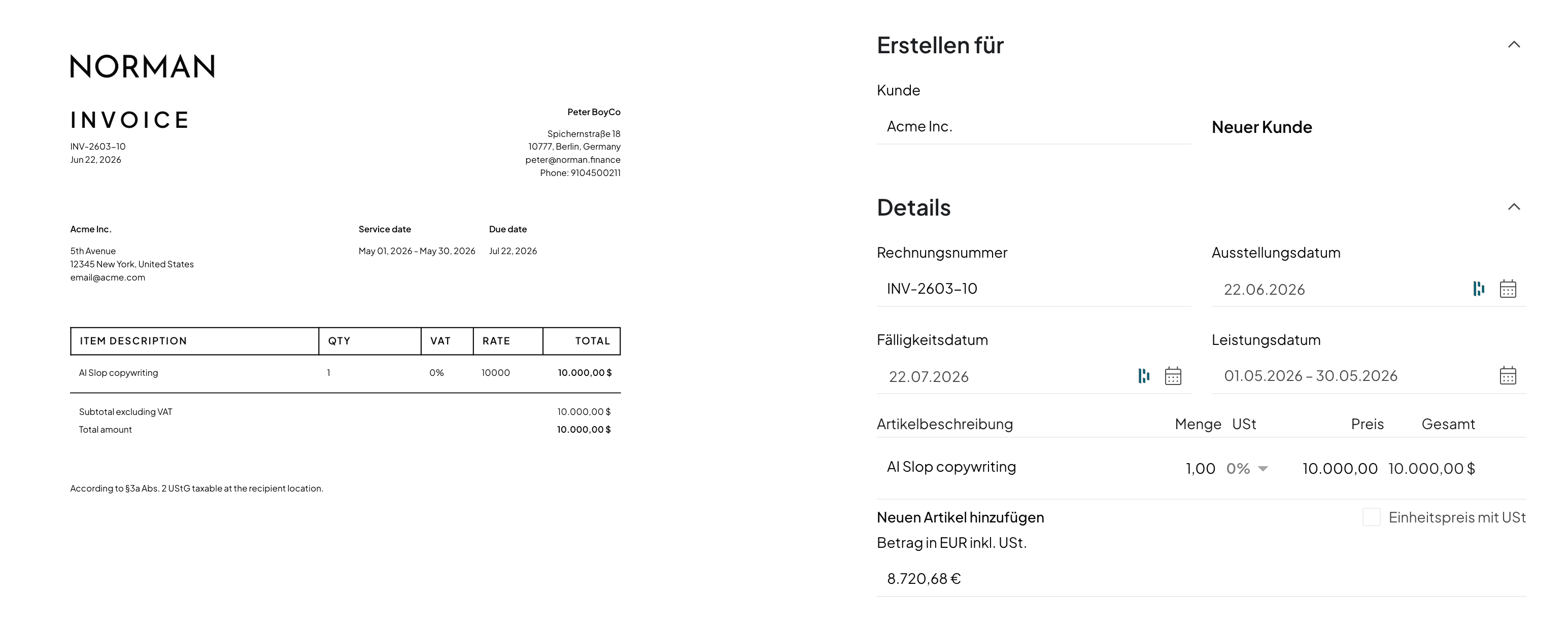

Required fields on a third-country invoice

Most of the mandatory invoice fields under § 14 Abs. 4 UStG still apply, with one specific around the VAT note:

- Full names and addresses of both seller and the non-EU customer

- Your German tax number (Steuernummer) or VAT ID (USt-IdNr.) (there is no customer EU VAT ID in a third country, and none is needed)

- Sequential invoice number, invoice date, service or delivery date

- Description of the service or goods, net amount (no German VAT line)

- The matching VAT note from the table above

A small-value invoice with reduced fields isn't advisable in cross-border B2B, write the full invoice instead, so your evidence for the tax office is clean.

Free invoice template (PDF, Word & Excel)

Legally compliant with all mandatory fields under §14 UStG, three formats, ready to use.

B2B vs. B2C: caution with private non-EU customers

Non-EU B2B is usually straightforward: no German VAT, a clear note on the invoice, done. B2C is trickier. For electronically supplied services (SaaS, digital products, online courses, e-books) to private customers outside the EU, local tax rules in the customer's country often apply. If you sell regularly to US consumers, US sales tax may become relevant in some states above certain thresholds; Switzerland and the UK have their own registration thresholds.

Important distinction: for EU consumers there's the OSS procedure, through which you remit the foreign VAT centrally. For third countries there is no such thing, if a local tax obligation arises, you handle it directly in that country or bring in a local tax adviser.

Converting foreign currency

You can invoice in any currency, EUR, USD, GBP, CHF. But your books and VAT must be in euros. Under § 16 Abs. 6 UStG, the relevant rate is the official monthly average rate published by the German Federal Ministry of Finance (the "VAT conversion rates" the BMF announces each month). Alternatively, the daily rate (e.g. the ECB reference rate) on the day of supply is allowed.

This applies even when the customer pays in foreign currency. The rate almost always moves between invoicing and payment, you book these currency differences as other operating income or expense, not as an adjustment to the sale.

Bookkeeping & VAT return: the right line

This is where the costliest mistakes happen, because "not taxable" and "exempt" are not the same thing. In SKR03/SKR04 there are dedicated accounts, and in the VAT return the two cases belong in different lines:

| Transaction | VAT-return line | Code | Typical SKR03 account |

|---|---|---|---|

| VAT-exempt goods export (§ 6 UStG) | line 24 | 43 | 8120 |

| Non-taxable B2B service (place of supply in third country) | line 41 | 45 | 8338 |

For Norman customers (mostly agencies, consultants and SaaS providers) line 41 (code 45) is almost always the right one: the non-taxable service. Line 24 (code 43) is for physical goods exports. You keep your input VAT deduction on your own incoming invoices in both cases, third-country sales do not block input VAT.

In Norman's AI bookkeeping receipts land on the right account and the right VAT-return line automatically once the customer address is recognised as a third country.

Export proof: only for goods exports

If you sell goods to a third country, the supply is only VAT-exempt if you provide export proof. Since the electronic ATLAS procedure was introduced, this runs via an electronic export declaration: it's mandatory above a goods value of €1,000 (or 1,000 kg); below that an oral declaration at the customs office of exit usually suffices. As proof you receive the exit certificate as a PDF after the goods cross the border, keep it for your books.

For pure services you need no export proof, what matters is that your customer is a business in the third country. You can show that with a commercial register extract, a business certificate or the correspondence.

Common mistakes on third-country invoices

- German VAT charged. For non-EU B2B there's no VAT on the invoice, charge 19% anyway and you owe it under § 14c UStG.

- VAT note forgotten. Without the note the invoice is formally incomplete and the customer complains.

- "Not taxable" confused with "exempt" and so the wrong VAT-return line chosen.

- EC Sales List filed. The EC Sales List only covers the EU, for third-country sales it's simply wrong.

- Foreign currency booked at the payment rate instead of the official rate on the day of supply.

Frequently asked questions

Do I charge VAT on a third-country invoice?

No. For B2B services the supply is not subject to German VAT (§ 3a Abs. 2 UStG), and for goods exports it's exempt (§ 6 UStG). In both cases you show the net amount and add the matching VAT note.

What note goes on an invoice to Switzerland or the US?

For services: "Not subject to German VAT (§ 3a Abs. 2 UStG)". For goods exports: "VAT-exempt export under § 6 UStG". If the third country has a reverse-charge system, add "Reverse charge".

Do I need a VAT ID for third-country customers?

No. The EU VAT ID only exists inside the EU. In a third country your own tax number or VAT ID on the invoice is enough; you don't need a number from the customer.

Do I report third-country sales in the EC Sales List?

No. The EC Sales List only concerns intra-community (EU) supplies. You enter third-country sales only in the VAT return, goods exports in line 24, non-taxable services in line 41.

Which currency can I invoice in?

Any. But for your books and VAT you convert the amount to euros at the official monthly BMF rate (or the daily rate on the day of supply). Currency differences up to payment are booked separately as income or expense.

Can I invoice a third country as a small business (Kleinunternehmer)?

Yes. As a small business under § 19 UStG you charge no VAT anyway, so little changes for third-country invoices. You keep the small-business note on the invoice.

Conclusion

Third-country invoicing isn't complicated once you know the basics: no German VAT for non-EU B2B, the right note depending on service vs. goods export, and the correct line in the VAT return, line 41 for non-taxable services, line 24 for VAT-exempt exports. Get the required fields right, convert foreign currency at the official rate, and remember: no EC Sales List, no OSS in a third country. With the right software the compliance side handles itself, and you keep selling globally.

Third-country invoices without VAT mistakes

Norman detects the third country from the customer address, adds the right VAT note automatically, converts foreign currency at the official rate and books the sale to the correct UStVA line, non-taxable service or VAT-exempt export. Your VAT return stays clean, whether the client is a US agency, a Swiss group or a UK company.