How to Correct a German VAT Return (UStVA) in 2026

VAT-return mistakes happen – what matters is fixing them properly. Here's how to file a correction in ELSTER without crossing into a Selbstanzeige under §371 AO.

- Category

- Taxes

- Updated

- Author

- Diana Chebotareva

Already filed your UStVA and realised a receipt's missing or a revenue line is wrong? Don't panic, corrections are routine and take five minutes in ELSTER. What you do need to know: at what point an innocent correction crosses into voluntary disclosure (Selbstanzeige under §371 AO), and why the VAT advance return follows its own, far more relaxed rulebook.

Quick answer

- How: In ELSTER, open the old UStVA, tick "Berichtigte Anmeldung" in line 10, re-enter all values, submit. The corrected return fully replaces the old one.

- Obligation, not option: The moment you spot an error that led to too little tax, you must correct it under §153 AO, without undue delay.

- Selbstanzeige risk: Only relevant if the error was deliberate or grossly negligent. Simple carelessness stays a harmless correction.

- The UStVA special case: Thanks to §371 Abs. 2a AO, you may correct advance returns repeatedly and even partially without losing criminal immunity, a privilege the annual return does not have.

- Costs: Late-payment surcharge 1 % per month, late-payment interest 1.8 % per year (after a 15-month grace period), and 6 % evasion interest if the shortfall was intentional.

When do you have to correct?

If you spot an error after filing that resulted in too little VAT charged or too much input VAT claimed, you're legally required to correct it under §153 of the German Tax Code (Abgabenordnung, AO). This covers:

- Forgotten invoices or postings

- Wrong VAT rates (7 % instead of 19 %)

- Double-claimed input VAT

- Wrong tax base due to credit notes or cancellations

- Advance payments booked into the wrong period

Important: if the error went against you (you overpaid), you're allowed to correct it, but not obliged. You almost always should: you get the money back as an input-VAT refund.

§153 AO, §371 AO or §378 AO: the decisive difference

Which provision applies depends solely on how the error arose, not on how big it is. This is the single most important distinction of the whole topic:

| Provision | When it applies | Consequence |

|---|---|---|

| §153 AO – correction | Simple, negligent error you notice later | Pure correction, no criminal or fine proceedings |

| §378 AO – reckless tax shortfall | Gross negligence (e.g. receipts ignored) | Fine possible; fine-exempting disclosure under §378 Abs. 3 AO |

| §371 AO – voluntary disclosure | Intentional understating | Immunity only with complete, timely disclosure + payment |

If you simply overlooked a receipt, you're safely in §153 territory. Only when you deliberately left revenue out does the correction count as a voluntary disclosure in criminal-law terms. In practice the line between "carelessness" and "reckless" is fluid, which is why the rule always holds: correct voluntarily and completely, before the Finanzamt finds the error itself.

Step by step: correcting in ELSTER

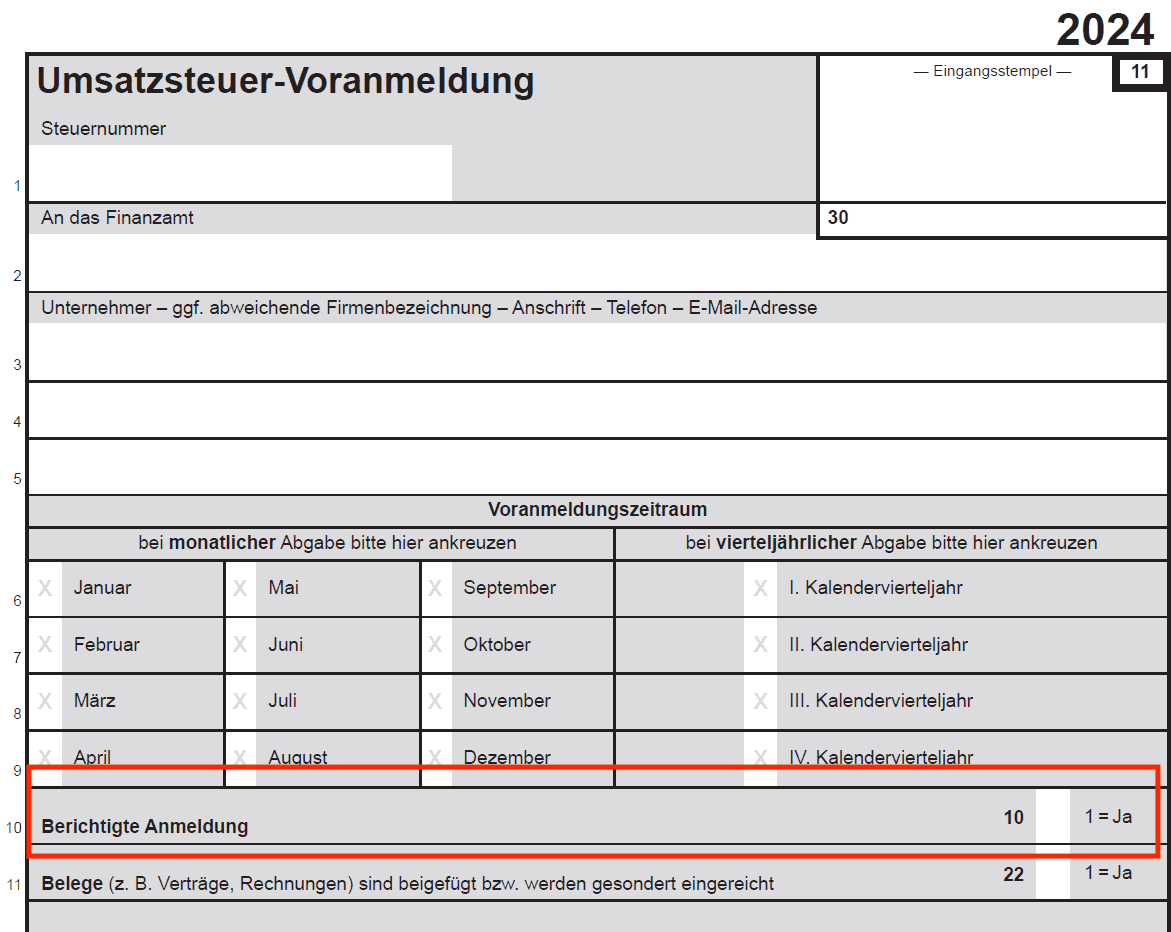

- Log into ELSTER and go to Mein ELSTER → Forms → Umsatzsteuer → UStVA. Pick the right period.

- Tick "Berichtigte Anmeldung" in line 10. This tells the tax office the new return replaces the old one, it doesn't add to it.

- Re-enter all values, not only the changed ones. ELSTER replaces the original UStVA completely; anything you omit counts as not reported.

- Submit, ELSTER shows the difference vs. the original.

- Pay the additional tax (or wait for the refund). On underpayments, a late-payment surcharge runs from the original due date.

Tip: with a permanent filing extension (Dauerfristverlängerung), the deadline shifts apply to corrections too. The general mechanics are covered in the complete VAT-return guide.

The UStVA special case: §371 Abs. 2a AO

This is the most important (and most misunderstood) point. For VAT advance returns, an exception under §371 Abs. 2a AO has applied since 1 January 2015:

- No completeness requirement: You don't have to fix every open error of every period in one go. A partial disclosure is again effective for the UStVA.

- Multiple corrections allowed: You may correct the same period a second time without losing criminal immunity.

- No €25,000 block: The threshold above which immunity is normally forfeited does not apply to the advance return.

In plain terms: a corrected advance return is far less dangerous than its reputation. The often-heard "correcting repeatedly looks suspicious" is not a legal problem but a purely practical observation, frequent corrections can draw a caseworker's attention and, in the extreme, trigger a special VAT audit. The correction still exempts you from prosecution.

It's different for the annual VAT return: there, the relief of §371 Abs. 2a AO does not apply. The full completeness requirement and the €25,000 threshold are back in force. That's exactly why you should clear errors in the relevant advance-return period, and not push them to the annual return.

The 3 most common VAT-return errors

90 %+ of cases boil down to:

- Wrong tax rate, 7 % vs. 19 %, especially for food, books, hospitality, catering. Our checklist of common EÜR mistakes covers most cases.

- Forgotten or duplicate postings, usually because receipts get uploaded too late or to the wrong month.

- Improper input VAT claims, e.g. claiming VAT from an invoice that's missing mandatory information or a VAT ID.

Interest, surcharges and penalty premiums

What a late or understated UStVA really costs depends on how much time passes and whether intent was involved:

| Item | Amount | When it applies |

|---|---|---|

| Late-payment surcharge (§240 AO) | 1 % per started month | On overdue tax you don't pay on time |

| Late-payment interest (§233a AO) | 1.8 % per year (0.15 % / month) | Only after a 15-month grace period, usually via the annual return |

| Evasion interest (§235 AO) | 6 % per year (0.5 % / month) | On intentional tax shortfalls |

| Penalty premium (§398a AO) | 10–20 % of the tax | On voluntary disclosures above €25,000 per offence |

The old §233a rate of 6 % per year no longer applies after the 2022 reform, the Constitutional Court struck it down. Late-payment and refund interest is now just 1.8 % per year, retroactively from 2019. The 6 % survived only for evasion interest (§235 AO).

Deadline: how long can you correct?

You can generally correct an advance return until you've filed the annual VAT return for the same year. A January UStVA can therefore still be corrected in November, as long as the annual return is still outstanding.

In theory you could roll all errors into the annual return. In practice, bad idea:

- The longer you wait, the sooner bigger discrepancies look like tax evasion.

- Late-payment interest accrues (1.8 % per year from month 15).

- The annual return loses the §371 Abs. 2a AO privilege, you give up the relaxed correction rules.

Rule of thumb: small errors from the most recent period (de-minimis ~€1,000) can usually be balanced in the next UStVA. Anything bigger, correct immediately and precisely.

Avoiding future errors

- Capture receipts immediately, not at month-end. With Norman, one photo per receipt is enough.

- Check the SKR account, quickly validate software suggestions.

- Mandatory invoice fields, address, VAT ID, service period. No input VAT recovery without a complete invoice.

- Don't file at the last hour, leave room to spot mistakes.

The UStVA is the only tax return that comes with an official "corrected" version. That alone tells you to fix mistakes the moment you spot them, and not drag them all the way to the annual reconciliation.

Peter BoykoFounder of Norman

Peter BoykoFounder of NormanFrequently asked questions

Can I correct a UStVA after filing at all?

Yes. You file a berichtigte Anmeldung (corrected return) for the same period in ELSTER (tick line 10). It fully replaces the original, a correction is possible even after the filing deadline.

How often may I correct the same UStVA?

For the advance return, as often as needed. Thanks to §371 Abs. 2a AO every correction stays exempt from prosecution, even if you revisit the same period repeatedly. Purely in practice: the more often you correct, the sooner a caseworker notices.

Does every correction automatically become a Selbstanzeige?

No. A voluntary disclosure only exists if the error was preceded by intent or gross negligence. A simply overlooked receipt is a pure §153 AO correction, with no criminal consequences.

What does a late payment cost me?

A late-payment surcharge of 1 % per started month on the open amount. Late-payment interest (1.8 % per year) only kicks in after a 15-month grace period, rare in day-to-day UStVA life.

Should I collect errors in the annual return instead?

No. The annual return follows the stricter rules (completeness requirement, €25,000 threshold). Fix errors in the relevant advance-return period while the favourable UStVA regime applies.

Bottom line

Correcting a UStVA is routine, and thanks to §371 Abs. 2a AO it's explicitly defused for the advance return: repeatedly, partially, with no amount cap. The real trap isn't the correction itself but doing nothing: a known error left for months can flip a harmless correction into a voluntary disclosure. With Norman for solo founders or Norman for GmbH, you've got clean bookings and accurately prepared UStVAs, the single best insurance against corrections.

Related reads: complete VAT return guide, VAT returns for GmbHs, tax-return mistakes.

Clean bookings are the best insurance against corrections

Norman validates every receipt, assigns VAT rates automatically and prepares your UStVA audit-ready, so you rarely need to correct it. And if you do, your data is already right.