Business Travel Expenses in Germany 2026: Mileage, Meals and Accommodation for Freelancers and GmbH Directors

Business travel costs in Germany are fully deductible for freelancers and GmbH managing directors. Here are the 2026 flat rates, accommodation rules, and what documentation you need.

- Category

- Taxes

- Updated

- Author

- Diana Chebotareva

Client visits, trade fairs, government appointments, business travel costs in Germany are fully deductible for freelancers and GmbH managing directors. The rules differ slightly depending on your legal structure, but the tax savings apply in either case. This article covers what counts as a travel expense, the 2026 flat rates, the most common calculation error, and what documentation you need.

Quick answer

- Travel expenses consist of four building blocks: transport, meal allowance, accommodation and incidental costs.

- Car: a flat €0.30 per kilometre driven, for every kilometre of the outbound and return trip. Don't confuse this with the tiered commuter rate (€0.30/€0.38), which applies only to the commute to your workplace.

- Domestic meal allowance 2026: €14 (8–24 hrs), €28 (full day), €14 each for arrival and departure days.

- Accommodation: the self-employed deduct only actual, documented costs, there is no flat overnight rate for them.

- GmbH managing directors: reimbursement via the GmbH is almost always better than the personal expense deduction.

What counts as business travel expenses?

Travel expenses arise when you leave your primary workplace for a business reason, a so-called temporary work assignment (Auswärtstätigkeit). The tax office splits them into four categories:

| Building block | Examples |

|---|---|

| Transport | Car, train, flight, taxi, rental car, public transport |

| Meal allowance | Per diem (flat rate) for meals while travelling |

| Accommodation | Hotel, guesthouse, Airbnb (against receipt) |

| Incidental costs | Parking, tolls, luggage, business phone calls |

All four are deductible in full as business expenses. What matters is the business purpose: a trip that is mostly private (e.g. a trade fair followed by a weekend holiday) has to be apportioned.

Travel expense or commuter allowance? The key distinction

This is where the costliest mistake happens. Trips between home and your regular place of business are not travel expenses, they fall under the commuter deduction (Entfernungspauschale): €0.30 for the first 20 km and €0.38 from the 21st km, but only for the one-way distance.

Genuine business trips, by contrast, use the travel mileage rate of a flat €0.30 per kilometre for the entire distance driven, outbound and return, with no tiering and no cap. Anyone who accidentally applies the tiered €0.38 is calculating it wrong. More on the distinction in our guide to the commuter allowance for the self-employed.

Transport: mileage rate 2026

If you use your private vehicle for business, you can claim a flat rate per kilometre that covers all running costs (fuel, insurance, maintenance, depreciation):

| Vehicle | Rate per km |

|---|---|

| Car | €0.30 |

| Motorcycle / scooter | €0.20 |

Example: A business trip of 120 km (one way) means 240 km there and back × €0.30 = €72 in transport costs, deductible tax-free, with no receipts at all.

Alternatively you can keep a mileage log (Fahrtenbuch) and claim actual vehicle costs. This is worthwhile for higher-value or heavily used cars, but it is documentation-intensive. GmbH-owned vehicles are booked through the company's assets anyway, the details are in our guide to the company car in a GmbH. Train, flight and taxi costs are always claimed at actual cost against a receipt.

Meal allowance (Verpflegungsmehraufwand) 2026

For the extra cost of eating while travelling there are fixed flat rates, no receipts needed. It doesn't matter how much you actually spent. Domestic rates remain unchanged for 2026:

| Absence | Allowance |

|---|---|

| 8 to 24 hours (single day) | €14 |

| full calendar day (24 hrs) | €28 |

| arrival and departure day (multi-day) | €14 each |

More on this (with worked examples, all foreign per-diem rates and an FAQ) in our focused guide to the meal allowance in Germany 2026.

Reduction when meals are provided

If a meal is provided for you (a hotel breakfast, say, or a business dinner someone else pays for) you have to reduce the daily allowance:

| Meal | Reduction | Amount |

|---|---|---|

| Breakfast | 20 % | −€5.60 |

| Lunch | 40 % | −€11.20 |

| Dinner | 40 % | −€11.20 |

If breakfast and dinner are both included in the hotel price on a full travel day, only €28 − €5.60 − €11.20 = €11.20 of the allowance remains.

The three-month rule

The meal allowance is only available for the first three months of a longer assignment at the same location. After that it lapses, because the site is treated like a regular workplace for tax purposes. A break of at least four weeks restarts the clock.

Note: the per diem only covers the extra cost of your own meals. If you invite business partners to dinner, those are entertainment expenses (Bewirtungskosten), deductible at 70 % under different rules. Details in our guide to deducting entertainment expenses.

Foreign travel: per diem and accommodation

For trips abroad, the Federal Ministry of Finance (BMF) publishes country-specific rates each year. Several were adjusted as of 1 January 2026. An extract (meals):

| Country / city | full day | arrival/departure |

|---|---|---|

| Austria | €50 | €33 |

| France (Paris) | €58 | €39 |

| Netherlands | €58 | €39 |

| Switzerland | €70 | €47 |

| Italy (Rome) | €48 | €32 |

| Spain (Madrid) | €42 | €28 |

| USA (New York) | €66 | €44 |

| United Kingdom (London) | €66 | €44 |

| Poland (Warsaw) | €40 | €27 |

For single-day trips abroad, the rate of the last foreign place of work applies. For overnight stays abroad there are flat rates too, but only an employer may apply them in a tax-free reimbursement. The self-employed (and employees claiming a deduction) always use the actual hotel bill.

Deducting accommodation correctly

Hotel costs are deductible at actual cost. You need a receipt addressed to the GmbH if the company pays, or to your own name as a freelancer. Two pitfalls:

- Strip out breakfast: if breakfast isn't shown separately, you have to deduct a flat €5.60 per day from the hotel bill, it is covered by the meal allowance instead.

- Three-month rule at the same place: staying at the same location for more than three consecutive months causes the tax office to increasingly treat it as a new primary workplace, reducing allowable deductions.

Don't forget incidental costs

Incidental travel costs are often overlooked but add up. Fully deductible items include: parking and tolls, luggage storage, rental-car extras, business-related phone and internet costs on the road, and travel luggage insurance. Importantly, parking fees are not covered by the mileage rate, they count separately.

The starter book for your self-employment

Free e-book: registration, accounting, your first invoice, and taxes, plus a tax calendar, deductions cheat sheet, and invoice template.

Special rules for GmbH managing directors

As a GmbH managing director you have two options:

- The GmbH reimburses your travel costs directly, a business expense for the company, a tax-free reimbursement for you.

- You bear the costs yourself and claim them as employment expenses (Werbungskosten) in your personal tax return.

Option 1 is almost always better. The GmbH saves corporate and trade tax on the amount, and you receive the money back entirely tax-free. The condition is a proper travel expense report. With the deduction route (option 2), the cost only takes effect via your personal tax rate, and only to the extent your employment expenses exceed the lump-sum allowance.

Travel expense report and documentation

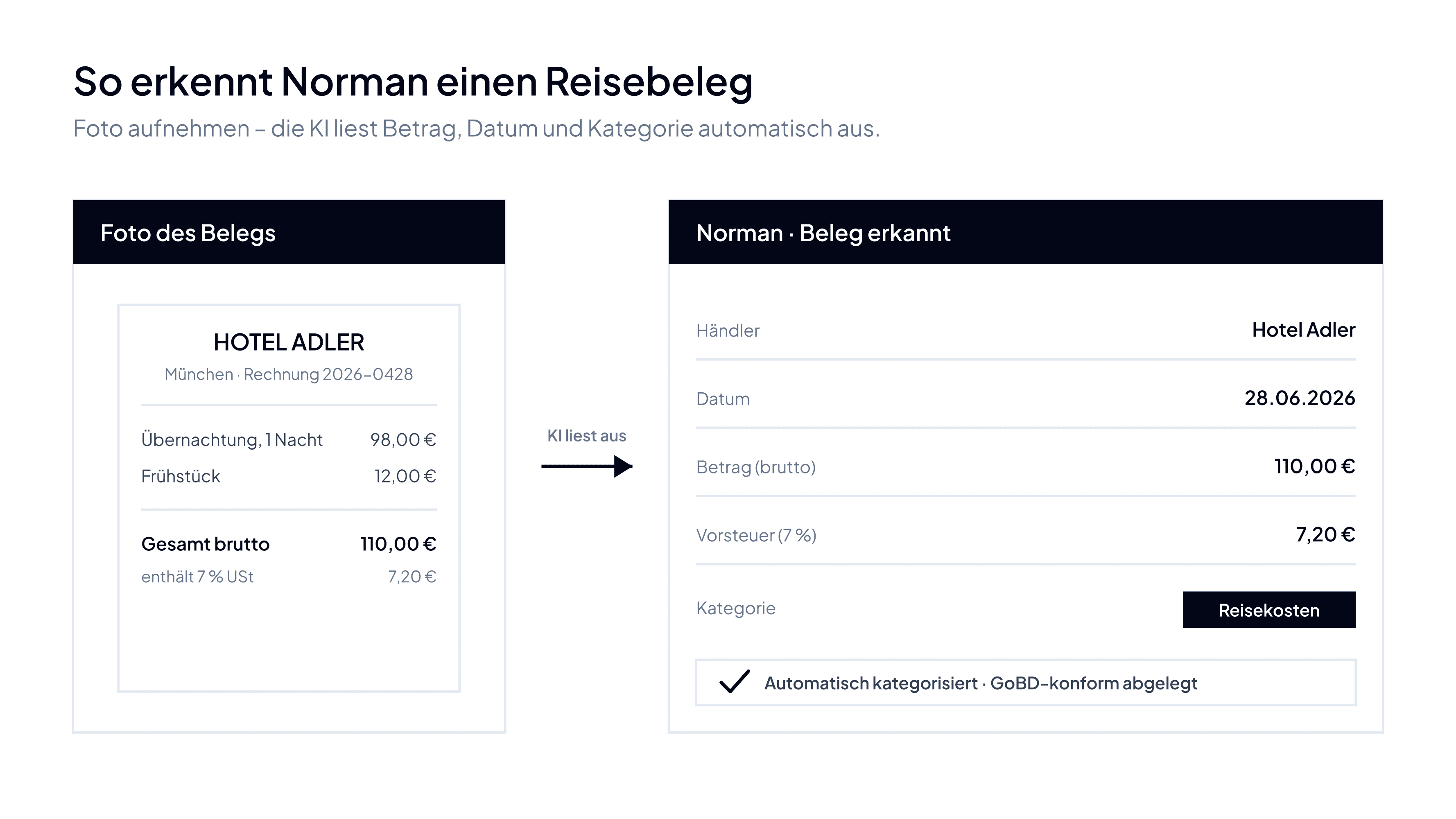

For every business trip you need a traceable report with: the date, destination and business purpose, the kilometres driven (for a car), plus receipts for accommodation and incidentals. All documents must be kept for 10 years, GoBD-compliant.

With Norman you photograph your hotel bill, parking ticket and fuel receipt straight into your bookkeeping, the AI reads the amount, categorises it as a travel expense and files the receipt audit-proof. Learn about AI Bookkeeping →

Frequently asked questions about travel expenses

How much mileage can I claim as a self-employed person?

For business trips, a flat €0.30 per kilometre driven, for the complete round trip, with no tiering. The tiered €0.30/€0.38 rates apply only to the commute to your own place of business (commuter allowance).

Do I need receipts for the meal allowance?

No. The per diem (€14 or €28) is a flat rate and is granted regardless of what you actually spent on food. You only need receipts for transport, accommodation and incidental costs.

Can a self-employed person claim a flat overnight rate?

No. The overnight flat rates apply only to tax-free reimbursement by an employer. The self-employed claim only the actual, documented hotel costs.

What happens after three months at the same location?

After three continuous months at the same site, the meal allowance lapses. A break of at least four weeks restarts the three-month clock.

Is the trip between home and office a travel expense?

No. That is the commute and falls under the commuter allowance, not travel expenses, a frequently confused point.

Bottom line

Business travel expenses are a valuable deduction for freelancers and GmbH managing directors. Mileage rates, meal allowances and accommodation costs add up quickly. Two things matter: apply the right rate (a flat €0.30/km, not the tiered commuter allowance) and document carefully. Then you will have no trouble at a tax audit.

Capture travel expenses by photo – Norman does the math

Photograph your hotel bill, parking ticket and fuel receipt straight into Norman. The AI bookkeeping categorises every expense as a business cost, calculates your mileage and meal allowances, and files everything GoBD-compliant for a tax audit. Invoicing and bookkeeping are free.