" height="89.58999999999997px" id="ngWGpRyVF" width="277.7205315341729px"/><path d="M 10.59 9.36 C 12.15 9.36 13.56 9.72 14.81 10.45 C 16.06 11.18 17.04 12.2 17.74 13.52 C 18.44 14.84 18.79 16.37 18.79 18.1 C 18.79 21.13 17.88 23.46 16.05 25.08 C 14.22 26.7 11.46 27.51 7.76 27.51 C 4.59 27.51 2.01 27.02 0 26.04 L 0 20.03 C 1.08 20.53 2.29 20.93 3.65 21.25 C 5 21.57 6.17 21.73 7.15 21.73 C 8.51 21.73 9.56 21.44 10.29 20.87 C 11.02 20.29 11.38 19.44 11.38 18.32 C 11.38 17.28 11.01 16.47 10.27 15.89 C 9.53 15.31 8.4 15.02 6.89 15.02 C 5.74 15.02 4.5 15.24 3.16 15.67 L 0.47 14.33 L 1.49 0 L 16.97 0 L 16.97 6.11 L 7.73 6.11 L 7.4 9.69 C 8.36 9.5 9.05 9.4 9.46 9.38 C 9.87 9.36 10.24 9.36 10.59 9.36 Z" fill="rgb(104, 197, 237)" height="27.50999999999999px" id="gcv_9jMLc" transform="translate(229.5 31)" width="18.789999999999992px"/><g d="M 51.28 14.45 C 51.81 13.62 52.51 12.94 53.38 12.42 C 54.25 11.9 55.33 11.64 56.62 11.64 C 57.35 11.64 58.02 11.72 58.61 11.89 C 59.2 12.05 59.73 12.26 60.2 12.5 C 60.67 12.74 61.09 13.02 61.47 13.33 C 61.85 13.65 62.19 13.96 62.49 14.26 C 62.94 13.83 63.36 13.36 63.74 12.86 C 64.12 12.36 64.31 11.85 64.31 11.34 C 64.31 11.01 64.23 10.71 64.06 10.43 C 63.9 10.15 63.7 9.91 63.47 9.71 C 63.27 9.53 62.97 9.31 62.58 9.05 C 62.19 8.78 61.7 8.53 61.1 8.29 C 60.51 8.05 59.81 7.84 59.02 7.66 C 58.22 7.48 57.33 7.39 56.35 7.39 C 54.35 7.39 52.62 7.73 51.14 8.39 C 49.66 9.06 48.43 9.99 47.45 11.17 C 46.47 12.36 45.73 13.77 45.23 15.39 C 44.74 17.02 44.49 18.79 44.49 20.71 C 44.49 22.63 44.72 24.39 45.17 25.99 C 45.62 27.59 46.34 28.98 47.31 30.16 C 48.28 31.33 49.51 32.25 51 32.91 C 52.49 33.57 54.26 33.89 56.3 33.89 C 57.36 33.89 58.3 33.81 59.12 33.64 C 59.94 33.48 60.64 33.28 61.2 33.05 C 61.77 32.82 62.23 32.6 62.58 32.37 C 62.93 32.14 63.19 31.95 63.34 31.8 C 63.62 31.52 63.82 31.27 63.95 31.04 C 64.08 30.81 64.14 30.54 64.14 30.21 C 64.14 29.98 64.08 29.73 63.95 29.45 C 63.82 29.17 63.67 28.89 63.5 28.62 C 63.32 28.34 63.13 28.08 62.93 27.82 C 62.73 27.57 62.55 27.35 62.4 27.18 C 62.17 27.38 61.89 27.62 61.55 27.9 C 61.21 28.18 60.81 28.44 60.36 28.7 C 59.91 28.95 59.38 29.17 58.79 29.34 C 58.2 29.52 57.55 29.61 56.84 29.61 C 55.5 29.61 54.38 29.36 53.49 28.85 C 52.611 28.367 51.863 27.677 51.31 26.84 C 50.75 26.01 50.36 25.05 50.14 23.96 C 49.91 22.87 49.8 21.74 49.8 20.55 C 49.8 19.44 49.91 18.35 50.14 17.27 C 50.37 16.24 50.75 15.29 51.28 14.45 Z M 82.89 21.77 C 82.89 20.6 82.76 19.58 82.51 18.7 C 82.26 17.82 81.83 17.09 81.23 16.51 C 80.63 15.93 79.86 15.49 78.9 15.21 C 77.95 14.93 76.78 14.79 75.41 14.79 C 74.42 14.79 73.48 14.87 72.59 15.04 C 71.7 15.21 70.91 15.42 70.23 15.69 C 69.54 15.96 69 16.26 68.61 16.59 C 68.22 16.92 68.02 17.26 68.02 17.62 C 68.02 17.87 68.13 18.26 68.34 18.78 C 68.56 19.3 68.84 19.78 69.2 20.21 C 70.01 19.75 70.84 19.35 71.7 18.99 C 72.55 18.63 73.52 18.46 74.62 18.46 C 75.79 18.46 76.63 18.67 77.15 19.08 C 77.67 19.49 77.93 20.18 77.93 21.16 L 77.93 21.85 L 77.11 21.85 C 76.82 21.85 76.52 21.86 76.21 21.89 C 75.3 21.94 74.29 22.05 73.2 22.23 C 72.11 22.41 71.09 22.73 70.15 23.2 C 69.21 23.67 68.43 24.31 67.81 25.12 C 67.19 25.93 66.88 26.98 66.88 28.27 C 66.88 29.31 67.06 30.19 67.41 30.91 C 67.77 31.63 68.22 32.21 68.78 32.64 C 69.34 33.07 69.96 33.38 70.65 33.57 C 71.34 33.76 72.02 33.85 72.71 33.85 C 74.03 33.85 75.15 33.65 76.06 33.24 C 76.97 32.83 77.71 32.34 78.27 31.75 C 78.4 32.41 78.7 32.92 79.17 33.27 C 79.64 33.63 80.33 33.8 81.25 33.8 C 81.68 33.8 82.09 33.76 82.49 33.69 C 82.88 33.61 83.31 33.49 83.77 33.31 C 83.19 32.4 82.89 30.93 82.89 28.93 Z M 78.01 28.41 C 78.01 28.61 77.91 28.84 77.72 29.08 C 77.53 29.32 77.27 29.54 76.94 29.75 C 76.61 29.95 76.23 30.12 75.8 30.25 C 75.37 30.38 74.91 30.44 74.43 30.44 C 73.46 30.44 72.78 30.19 72.37 29.7 C 71.96 29.2 71.76 28.6 71.76 27.89 C 71.76 27.26 71.91 26.73 72.22 26.33 C 72.52 25.92 72.92 25.59 73.4 25.34 C 73.88 25.09 74.43 24.91 75.06 24.81 C 75.68 24.71 76.31 24.63 76.95 24.58 C 77.13 24.55 77.31 24.54 77.48 24.54 L 78.01 24.54 Z M 102.48 16.82 C 101.82 16.11 101.07 15.59 100.22 15.28 C 99.363 14.958 98.455 14.796 97.54 14.8 C 96.22 14.8 95.13 15.05 94.27 15.54 C 93.41 16.04 92.78 16.53 92.37 17.01 C 92.22 16.35 91.84 15.88 91.26 15.6 C 90.67 15.32 89.95 15.18 89.11 15.18 C 88.83 15.18 88.59 15.19 88.38 15.2 C 88.18 15.21 88 15.23 87.84 15.26 C 87.66 15.29 87.51 15.31 87.38 15.34 L 87.38 41.48 L 92.56 41.48 L 92.56 32.11 C 92.61 32.19 92.74 32.33 92.94 32.53 C 93.14 32.73 93.43 32.94 93.81 33.14 C 94.19 33.34 94.65 33.53 95.2 33.69 C 95.74 33.85 96.38 33.94 97.12 33.94 C 98.01 33.94 98.89 33.79 99.78 33.48 C 100.67 33.18 101.47 32.65 102.19 31.9 C 102.91 31.15 103.5 30.13 103.96 28.85 C 104.42 27.57 104.64 25.93 104.64 23.95 C 104.64 22.25 104.44 20.81 104.05 19.64 C 103.67 18.47 103.14 17.53 102.48 16.82 Z M 98.33 28.33 C 97.72 29.35 96.78 29.85 95.49 29.85 C 94.81 29.85 94.21 29.71 93.69 29.43 C 93.17 29.15 92.81 28.91 92.61 28.71 L 92.61 20.63 C 92.61 20.15 92.82 19.7 93.24 19.3 C 93.66 18.89 94.4 18.69 95.46 18.69 C 96.17 18.69 96.77 18.82 97.26 19.09 C 97.75 19.36 98.14 19.73 98.44 20.21 C 98.73 20.69 98.94 21.26 99.07 21.93 C 99.2 22.59 99.26 23.3 99.26 24.06 C 99.24 25.89 98.94 27.31 98.33 28.33 Z M 118.52 28.56 C 118.44 28.64 118.31 28.75 118.12 28.9 C 117.93 29.05 117.71 29.2 117.45 29.34 C 117.2 29.48 116.91 29.61 116.59 29.72 C 116.27 29.83 115.94 29.89 115.58 29.89 C 114.13 29.89 113.41 29 113.41 27.23 L 113.41 19.1 L 118.75 19.1 L 118.75 15.25 L 113.41 15.25 L 113.41 12.54 C 113.41 11.91 113.31 11.39 113.11 11 C 112.91 10.61 112.64 10.29 112.31 10.07 C 111.98 9.84 111.61 9.69 111.2 9.61 C 110.79 9.53 110.39 9.5 109.98 9.5 C 109.78 9.5 109.57 9.51 109.37 9.52 C 109.17 9.53 108.98 9.55 108.8 9.58 C 108.6 9.61 108.41 9.63 108.23 9.66 L 108.23 27.34 C 108.23 27.9 108.26 28.46 108.31 29.02 C 108.36 29.58 108.47 30.11 108.65 30.62 C 109.01 31.61 109.62 32.41 110.5 33.02 C 111.38 33.63 112.6 33.93 114.18 33.93 C 114.99 33.93 115.74 33.85 116.43 33.68 C 117.12 33.51 117.7 33.3 118.18 33.03 C 118.66 32.76 119.04 32.47 119.3 32.15 C 119.57 31.83 119.7 31.5 119.7 31.17 C 119.7 30.81 119.6 30.43 119.4 30.02 C 119.2 29.6 118.9 29.12 118.52 28.56 Z M 136.53 17.26 C 135.91 16.51 135.1 15.91 134.11 15.47 C 133.12 15.03 131.91 14.8 130.49 14.8 C 129.4 14.8 128.33 14.98 127.29 15.33 C 126.25 15.69 125.31 16.24 124.49 17.01 C 123.66 17.77 123 18.73 122.51 19.89 C 122.02 21.05 121.77 22.42 121.77 24.03 C 121.77 25.99 122.05 27.61 122.61 28.89 C 123.17 30.17 123.9 31.2 124.8 31.96 C 125.7 32.72 126.73 33.26 127.89 33.56 C 129.05 33.86 130.22 34.02 131.42 34.02 C 132.74 34.02 133.89 33.87 134.87 33.58 C 135.85 33.29 136.6 32.94 137.14 32.53 C 137.77 32.07 138.09 31.56 138.09 31.01 C 138.09 30.63 137.92 30.14 137.59 29.54 C 137.26 28.94 136.94 28.45 136.63 28.07 C 136.4 28.27 136.15 28.5 135.86 28.74 C 135.58 28.98 135.25 29.2 134.87 29.41 C 134.49 29.61 134.05 29.79 133.57 29.92 C 133.09 30.06 132.52 30.13 131.89 30.13 C 130.23 30.13 129.02 29.67 128.26 28.74 C 127.5 27.81 127.06 26.65 126.96 25.25 L 138.2 25.25 C 138.22 25.12 138.24 24.95 138.26 24.74 C 138.27 24.52 138.29 24.3 138.3 24.07 C 138.31 23.84 138.32 23.63 138.32 23.42 L 138.32 22.89 C 138.32 21.82 138.18 20.81 137.9 19.84 C 137.61 18.86 137.16 18.01 136.53 17.26 Z M 126.91 22.38 C 126.91 21.08 127.22 20.07 127.85 19.35 C 128.48 18.63 129.31 18.26 130.36 18.26 C 131.59 18.26 132.44 18.64 132.91 19.4 C 133.38 20.16 133.62 21.15 133.62 22.37 L 126.91 22.37 Z M 153.44 15.16 C 153.15 15.02 152.83 14.93 152.49 14.88 C 152.15 14.83 151.82 14.8 151.52 14.8 C 151.01 14.8 150.53 14.88 150.09 15.03 C 149.65 15.18 149.24 15.37 148.87 15.6 C 148.5 15.83 148.19 16.08 147.94 16.36 C 147.69 16.64 147.48 16.89 147.33 17.12 C 147.18 16.47 146.8 15.98 146.21 15.67 C 145.61 15.36 144.91 15.2 144.09 15.2 C 143.81 15.2 143.57 15.21 143.37 15.22 C 143.17 15.23 142.99 15.25 142.84 15.28 C 142.66 15.31 142.51 15.33 142.38 15.36 L 142.38 33.96 L 147.56 33.96 L 147.56 21.59 C 147.56 20.95 147.83 20.4 148.36 19.95 C 148.89 19.49 149.55 19.26 150.34 19.26 C 150.92 19.26 151.43 19.36 151.86 19.55 C 152.29 19.74 152.72 20.01 153.16 20.37 C 153.44 19.86 153.72 19.25 154 18.53 C 154.28 17.81 154.42 17.17 154.42 16.62 C 154.42 16.27 154.33 15.97 154.15 15.73 C 153.97 15.48 153.74 15.3 153.44 15.16 Z M 168.18 15.16 C 167.89 15.02 167.57 14.93 167.23 14.88 C 166.89 14.83 166.56 14.8 166.26 14.8 C 165.75 14.8 165.28 14.88 164.83 15.03 C 164.39 15.18 163.98 15.37 163.61 15.6 C 163.24 15.83 162.93 16.08 162.68 16.36 C 162.43 16.64 162.22 16.89 162.07 17.12 C 161.92 16.47 161.54 15.98 160.95 15.67 C 160.35 15.36 159.65 15.2 158.83 15.2 C 158.55 15.2 158.31 15.21 158.11 15.22 C 157.91 15.23 157.73 15.25 157.58 15.28 C 157.4 15.31 157.25 15.33 157.12 15.36 L 157.12 33.96 L 162.3 33.96 L 162.3 21.59 C 162.3 20.95 162.57 20.4 163.1 19.95 C 163.63 19.49 164.29 19.26 165.08 19.26 C 165.66 19.26 166.17 19.36 166.6 19.55 C 167.03 19.74 167.46 20.01 167.9 20.37 C 168.18 19.86 168.46 19.25 168.74 18.53 C 169.02 17.81 169.16 17.17 169.16 16.62 C 169.16 16.27 169.07 15.97 168.89 15.73 C 168.71 15.48 168.47 15.3 168.18 15.16 Z M 186.8 28.94 L 186.8 21.77 C 186.8 20.6 186.67 19.58 186.42 18.7 C 186.17 17.82 185.74 17.09 185.14 16.51 C 184.54 15.93 183.77 15.49 182.82 15.21 C 181.87 14.93 180.7 14.79 179.33 14.79 C 178.34 14.79 177.4 14.87 176.51 15.04 C 175.62 15.21 174.83 15.42 174.15 15.69 C 173.46 15.96 172.92 16.26 172.53 16.59 C 172.14 16.92 171.94 17.26 171.94 17.62 C 171.94 17.87 172.05 18.26 172.26 18.78 C 172.48 19.3 172.76 19.78 173.12 20.21 C 173.93 19.75 174.76 19.35 175.62 18.99 C 176.47 18.63 177.44 18.46 178.54 18.46 C 179.71 18.46 180.55 18.67 181.07 19.08 C 181.59 19.49 181.85 20.18 181.85 21.16 L 181.85 21.85 L 181.03 21.85 C 180.74 21.85 180.44 21.86 180.13 21.89 C 179.22 21.94 178.21 22.05 177.12 22.23 C 176.03 22.41 175.01 22.73 174.07 23.2 C 173.13 23.67 172.35 24.31 171.73 25.12 C 171.11 25.93 170.8 26.98 170.8 28.27 C 170.8 29.31 170.98 30.19 171.33 30.91 C 171.69 31.63 172.14 32.21 172.7 32.64 C 173.26 33.07 173.88 33.38 174.57 33.57 C 175.26 33.76 175.94 33.85 176.63 33.85 C 177.95 33.85 179.07 33.65 179.98 33.24 C 180.89 32.83 181.63 32.34 182.19 31.75 C 182.32 32.41 182.62 32.92 183.09 33.27 C 183.56 33.63 184.25 33.8 185.17 33.8 C 185.6 33.8 186.01 33.76 186.41 33.69 C 186.8 33.61 187.23 33.49 187.69 33.31 C 187.09 32.41 186.8 30.95 186.8 28.94 Z M 181.92 28.41 C 181.92 28.61 181.82 28.84 181.63 29.08 C 181.44 29.32 181.18 29.54 180.85 29.75 C 180.52 29.95 180.14 30.12 179.71 30.25 C 179.28 30.38 178.82 30.44 178.34 30.44 C 177.37 30.44 176.69 30.19 176.28 29.7 C 175.87 29.2 175.67 28.6 175.67 27.89 C 175.67 27.26 175.82 26.73 176.13 26.33 C 176.43 25.92 176.83 25.59 177.31 25.34 C 177.79 25.09 178.35 24.91 178.97 24.81 C 179.59 24.71 180.22 24.63 180.86 24.58 C 181.04 24.55 181.22 24.54 181.39 24.54 L 181.92 24.54 Z M 19.88 21.98 L 0 15.25 L 27.66 4.89 L 40.72 0 L 27.66 41.47 Z" fill="transparent" height="41.47999983131143px" id="kfVsvx2jF" transform="translate(4.5 9.5)" width="187.6899992370606px"><path d="M 6.79 7.06 C 7.32 6.23 8.02 5.55 8.89 5.03 C 9.76 4.51 10.84 4.25 12.13 4.25 C 12.86 4.25 13.53 4.33 14.12 4.5 C 14.71 4.66 15.24 4.87 15.71 5.11 C 16.18 5.35 16.6 5.63 16.98 5.94 C 17.36 6.26 17.7 6.57 18 6.87 C 18.45 6.44 18.87 5.97 19.25 5.47 C 19.63 4.97 19.82 4.46 19.82 3.95 C 19.82 3.62 19.74 3.32 19.57 3.04 C 19.41 2.76 19.21 2.52 18.98 2.32 C 18.78 2.14 18.48 1.92 18.09 1.66 C 17.7 1.39 17.21 1.14 16.61 0.9 C 16.02 0.66 15.32 0.45 14.53 0.27 C 13.73 0.09 12.84 0 11.86 0 C 9.86 0 8.13 0.34 6.65 1 C 5.17 1.67 3.94 2.6 2.96 3.78 C 1.98 4.97 1.24 6.38 0.74 8 C 0.25 9.63 0 11.4 0 13.32 C 0 15.24 0.23 17 0.68 18.6 C 1.13 20.2 1.85 21.59 2.82 22.77 C 3.79 23.94 5.02 24.86 6.51 25.52 C 8 26.18 9.77 26.5 11.81 26.5 C 12.87 26.5 13.81 26.42 14.63 26.25 C 15.45 26.09 16.15 25.89 16.71 25.66 C 17.28 25.43 17.74 25.21 18.09 24.98 C 18.44 24.75 18.7 24.56 18.85 24.41 C 19.13 24.13 19.33 23.88 19.46 23.65 C 19.59 23.42 19.65 23.15 19.65 22.82 C 19.65 22.59 19.59 22.34 19.46 22.06 C 19.33 21.78 19.18 21.5 19.01 21.23 C 18.83 20.95 18.64 20.69 18.44 20.43 C 18.24 20.18 18.06 19.96 17.91 19.79 C 17.68 19.99 17.4 20.23 17.06 20.51 C 16.72 20.79 16.32 21.05 15.87 21.31 C 15.42 21.56 14.89 21.78 14.3 21.95 C 13.71 22.13 13.06 22.22 12.35 22.22 C 11.01 22.22 9.89 21.97 9 21.46 C 8.121 20.977 7.373 20.287 6.82 19.45 C 6.26 18.62 5.87 17.66 5.65 16.57 C 5.42 15.48 5.31 14.35 5.31 13.16 C 5.31 12.05 5.42 10.96 5.65 9.88 C 5.88 8.85 6.26 7.9 6.79 7.06 Z M 38.4 14.38 C 38.4 13.21 38.27 12.19 38.02 11.31 C 37.77 10.43 37.34 9.7 36.74 9.12 C 36.14 8.54 35.37 8.1 34.41 7.82 C 33.46 7.54 32.29 7.4 30.92 7.4 C 29.93 7.4 28.99 7.48 28.1 7.65 C 27.21 7.82 26.42 8.03 25.74 8.3 C 25.05 8.57 24.51 8.87 24.12 9.2 C 23.73 9.53 23.53 9.87 23.53 10.23 C 23.53 10.48 23.64 10.87 23.85 11.39 C 24.07 11.91 24.35 12.39 24.71 12.82 C 25.52 12.36 26.35 11.96 27.21 11.6 C 28.06 11.24 29.03 11.07 30.13 11.07 C 31.3 11.07 32.14 11.28 32.66 11.69 C 33.18 12.1 33.44 12.79 33.44 13.77 L 33.44 14.46 L 32.62 14.46 C 32.33 14.46 32.03 14.47 31.72 14.5 C 30.81 14.55 29.8 14.66 28.71 14.84 C 27.62 15.02 26.6 15.34 25.66 15.81 C 24.72 16.28 23.94 16.92 23.32 17.73 C 22.7 18.54 22.39 19.59 22.39 20.88 C 22.39 21.92 22.57 22.8 22.92 23.52 C 23.28 24.24 23.73 24.82 24.29 25.25 C 24.85 25.68 25.47 25.99 26.16 26.18 C 26.85 26.37 27.53 26.46 28.22 26.46 C 29.54 26.46 30.66 26.26 31.57 25.85 C 32.48 25.44 33.22 24.95 33.78 24.36 C 33.91 25.02 34.21 25.53 34.68 25.88 C 35.15 26.24 35.84 26.41 36.76 26.41 C 37.19 26.41 37.6 26.37 38 26.3 C 38.39 26.22 38.82 26.1 39.28 25.92 C 38.7 25.01 38.4 23.54 38.4 21.54 Z M 33.52 21.02 C 33.52 21.22 33.42 21.45 33.23 21.69 C 33.04 21.93 32.78 22.15 32.45 22.36 C 32.12 22.56 31.74 22.73 31.31 22.86 C 30.88 22.99 30.42 23.05 29.94 23.05 C 28.97 23.05 28.29 22.8 27.88 22.31 C 27.47 21.81 27.27 21.21 27.27 20.5 C 27.27 19.87 27.42 19.34 27.73 18.94 C 28.03 18.53 28.43 18.2 28.91 17.95 C 29.39 17.7 29.94 17.52 30.57 17.42 C 31.19 17.32 31.82 17.24 32.46 17.19 C 32.64 17.16 32.82 17.15 32.99 17.15 L 33.52 17.15 Z M 57.99 9.43 C 57.33 8.72 56.58 8.2 55.73 7.89 C 54.873 7.568 53.965 7.406 53.05 7.41 C 51.73 7.41 50.64 7.66 49.78 8.15 C 48.92 8.65 48.29 9.14 47.88 9.62 C 47.73 8.96 47.35 8.49 46.77 8.21 C 46.18 7.93 45.46 7.79 44.62 7.79 C 44.34 7.79 44.1 7.8 43.89 7.81 C 43.69 7.82 43.51 7.84 43.35 7.87 C 43.17 7.9 43.02 7.92 42.89 7.95 L 42.89 34.09 L 48.07 34.09 L 48.07 24.72 C 48.12 24.8 48.25 24.94 48.45 25.14 C 48.65 25.34 48.94 25.55 49.32 25.75 C 49.7 25.95 50.16 26.14 50.71 26.3 C 51.25 26.46 51.89 26.55 52.63 26.55 C 53.52 26.55 54.4 26.4 55.29 26.09 C 56.18 25.79 56.98 25.26 57.7 24.51 C 58.42 23.76 59.01 22.74 59.47 21.46 C 59.93 20.18 60.15 18.54 60.15 16.56 C 60.15 14.86 59.95 13.42 59.56 12.25 C 59.18 11.08 58.65 10.14 57.99 9.43 Z M 53.84 20.94 C 53.23 21.96 52.29 22.46 51 22.46 C 50.32 22.46 49.72 22.32 49.2 22.04 C 48.68 21.76 48.32 21.52 48.12 21.32 L 48.12 13.24 C 48.12 12.76 48.33 12.31 48.75 11.91 C 49.17 11.5 49.91 11.3 50.97 11.3 C 51.68 11.3 52.28 11.43 52.77 11.7 C 53.26 11.97 53.65 12.34 53.95 12.82 C 54.24 13.3 54.45 13.87 54.58 14.54 C 54.71 15.2 54.77 15.91 54.77 16.67 C 54.75 18.5 54.45 19.92 53.84 20.94 Z M 74.03 21.17 C 73.95 21.25 73.82 21.36 73.63 21.51 C 73.44 21.66 73.22 21.81 72.96 21.95 C 72.71 22.09 72.42 22.22 72.1 22.33 C 71.78 22.44 71.45 22.5 71.09 22.5 C 69.64 22.5 68.92 21.61 68.92 19.84 L 68.92 11.71 L 74.26 11.71 L 74.26 7.86 L 68.92 7.86 L 68.92 5.15 C 68.92 4.52 68.82 4 68.62 3.61 C 68.42 3.22 68.15 2.9 67.82 2.68 C 67.49 2.45 67.12 2.3 66.71 2.22 C 66.3 2.14 65.9 2.11 65.49 2.11 C 65.29 2.11 65.08 2.12 64.88 2.13 C 64.68 2.14 64.49 2.16 64.31 2.19 C 64.11 2.22 63.92 2.24 63.74 2.27 L 63.74 19.95 C 63.74 20.51 63.77 21.07 63.82 21.63 C 63.87 22.19 63.98 22.72 64.16 23.23 C 64.52 24.22 65.13 25.02 66.01 25.63 C 66.89 26.24 68.11 26.54 69.69 26.54 C 70.5 26.54 71.25 26.46 71.94 26.29 C 72.63 26.12 73.21 25.91 73.69 25.64 C 74.17 25.37 74.55 25.08 74.81 24.76 C 75.08 24.44 75.21 24.11 75.21 23.78 C 75.21 23.42 75.11 23.04 74.91 22.63 C 74.71 22.21 74.41 21.73 74.03 21.17 Z M 92.04 9.87 C 91.42 9.12 90.61 8.52 89.62 8.08 C 88.63 7.64 87.42 7.41 86 7.41 C 84.91 7.41 83.84 7.59 82.8 7.94 C 81.76 8.3 80.82 8.85 80 9.62 C 79.17 10.38 78.51 11.34 78.02 12.5 C 77.53 13.66 77.28 15.03 77.28 16.64 C 77.28 18.6 77.56 20.22 78.12 21.5 C 78.68 22.78 79.41 23.81 80.31 24.57 C 81.21 25.33 82.24 25.87 83.4 26.17 C 84.56 26.47 85.73 26.63 86.93 26.63 C 88.25 26.63 89.4 26.48 90.38 26.19 C 91.36 25.9 92.11 25.55 92.65 25.14 C 93.28 24.68 93.6 24.17 93.6 23.62 C 93.6 23.24 93.43 22.75 93.1 22.15 C 92.77 21.55 92.45 21.06 92.14 20.68 C 91.91 20.88 91.66 21.11 91.37 21.35 C 91.09 21.59 90.76 21.81 90.38 22.02 C 90 22.22 89.56 22.4 89.08 22.53 C 88.6 22.67 88.03 22.74 87.4 22.74 C 85.74 22.74 84.53 22.28 83.77 21.35 C 83.01 20.42 82.57 19.26 82.47 17.86 L 93.71 17.86 C 93.73 17.73 93.75 17.56 93.77 17.35 C 93.78 17.13 93.8 16.91 93.81 16.68 C 93.82 16.45 93.83 16.24 93.83 16.03 L 93.83 15.5 C 93.83 14.43 93.69 13.42 93.41 12.45 C 93.12 11.47 92.67 10.62 92.04 9.87 Z M 82.42 14.99 C 82.42 13.69 82.73 12.68 83.36 11.96 C 83.99 11.24 84.82 10.87 85.87 10.87 C 87.1 10.87 87.95 11.25 88.42 12.01 C 88.89 12.77 89.13 13.76 89.13 14.98 L 82.42 14.98 Z M 108.95 7.77 C 108.66 7.63 108.34 7.54 108 7.49 C 107.66 7.44 107.33 7.41 107.03 7.41 C 106.52 7.41 106.04 7.49 105.6 7.64 C 105.16 7.79 104.75 7.98 104.38 8.21 C 104.01 8.44 103.7 8.69 103.45 8.97 C 103.2 9.25 102.99 9.5 102.84 9.73 C 102.69 9.08 102.31 8.59 101.72 8.28 C 101.12 7.97 100.42 7.81 99.6 7.81 C 99.32 7.81 99.08 7.82 98.88 7.83 C 98.68 7.84 98.5 7.86 98.35 7.89 C 98.17 7.92 98.02 7.94 97.89 7.97 L 97.89 26.57 L 103.07 26.57 L 103.07 14.2 C 103.07 13.56 103.34 13.01 103.87 12.56 C 104.4 12.1 105.06 11.87 105.85 11.87 C 106.43 11.87 106.94 11.97 107.37 12.16 C 107.8 12.35 108.23 12.62 108.67 12.98 C 108.95 12.47 109.23 11.86 109.51 11.14 C 109.79 10.42 109.93 9.78 109.93 9.23 C 109.93 8.88 109.84 8.58 109.66 8.34 C 109.48 8.09 109.25 7.91 108.95 7.77 Z M 123.69 7.77 C 123.4 7.63 123.08 7.54 122.74 7.49 C 122.4 7.44 122.07 7.41 121.77 7.41 C 121.26 7.41 120.79 7.49 120.34 7.64 C 119.9 7.79 119.49 7.98 119.12 8.21 C 118.75 8.44 118.44 8.69 118.19 8.97 C 117.94 9.25 117.73 9.5 117.58 9.73 C 117.43 9.08 117.05 8.59 116.46 8.28 C 115.86 7.97 115.16 7.81 114.34 7.81 C 114.06 7.81 113.82 7.82 113.62 7.83 C 113.42 7.84 113.24 7.86 113.09 7.89 C 112.91 7.92 112.76 7.94 112.63 7.97 L 112.63 26.57 L 117.81 26.57 L 117.81 14.2 C 117.81 13.56 118.08 13.01 118.61 12.56 C 119.14 12.1 119.8 11.87 120.59 11.87 C 121.17 11.87 121.68 11.97 122.11 12.16 C 122.54 12.35 122.97 12.62 123.41 12.98 C 123.69 12.47 123.97 11.86 124.25 11.14 C 124.53 10.42 124.67 9.78 124.67 9.23 C 124.67 8.88 124.58 8.58 124.4 8.34 C 124.22 8.09 123.98 7.91 123.69 7.77 Z M 142.31 21.55 L 142.31 14.38 C 142.31 13.21 142.18 12.19 141.93 11.31 C 141.68 10.43 141.25 9.7 140.65 9.12 C 140.05 8.54 139.28 8.1 138.33 7.82 C 137.38 7.54 136.21 7.4 134.84 7.4 C 133.85 7.4 132.91 7.48 132.02 7.65 C 131.13 7.82 130.34 8.03 129.66 8.3 C 128.97 8.57 128.43 8.87 128.04 9.2 C 127.65 9.53 127.45 9.87 127.45 10.23 C 127.45 10.48 127.56 10.87 127.77 11.39 C 127.99 11.91 128.27 12.39 128.63 12.82 C 129.44 12.36 130.27 11.96 131.13 11.6 C 131.98 11.24 132.95 11.07 134.05 11.07 C 135.22 11.07 136.06 11.28 136.58 11.69 C 137.1 12.1 137.36 12.79 137.36 13.77 L 137.36 14.46 L 136.54 14.46 C 136.25 14.46 135.95 14.47 135.64 14.5 C 134.73 14.55 133.72 14.66 132.63 14.84 C 131.54 15.02 130.52 15.34 129.58 15.81 C 128.64 16.28 127.86 16.92 127.24 17.73 C 126.62 18.54 126.31 19.59 126.31 20.88 C 126.31 21.92 126.49 22.8 126.84 23.52 C 127.2 24.24 127.65 24.82 128.21 25.25 C 128.77 25.68 129.39 25.99 130.08 26.18 C 130.77 26.37 131.45 26.46 132.14 26.46 C 133.46 26.46 134.58 26.26 135.49 25.85 C 136.4 25.44 137.14 24.95 137.7 24.36 C 137.83 25.02 138.13 25.53 138.6 25.88 C 139.07 26.24 139.76 26.41 140.68 26.41 C 141.11 26.41 141.52 26.37 141.92 26.3 C 142.31 26.22 142.74 26.1 143.2 25.92 C 142.6 25.02 142.31 23.56 142.31 21.55 Z M 137.43 21.02 C 137.43 21.22 137.33 21.45 137.14 21.69 C 136.95 21.93 136.69 22.15 136.36 22.36 C 136.03 22.56 135.65 22.73 135.22 22.86 C 134.79 22.99 134.33 23.05 133.85 23.05 C 132.88 23.05 132.2 22.8 131.79 22.31 C 131.38 21.81 131.18 21.21 131.18 20.5 C 131.18 19.87 131.33 19.34 131.64 18.94 C 131.94 18.53 132.34 18.2 132.82 17.95 C 133.3 17.7 133.86 17.52 134.48 17.42 C 135.1 17.32 135.73 17.24 136.37 17.19 C 136.55 17.16 136.73 17.15 136.9 17.15 L 137.43 17.15 Z" fill="rgb(0, 46, 71)" height="34.089999964825836px" id="fNaRY0pwf" stroke-dasharray="" stroke-linecap="butt" stroke-linejoin="round" stroke-width="3.262" stroke="rgb(0, 46, 71)" transform="translate(44.49 7.39)" width="143.1999975585938px"/><path d="M 19.88 21.98 L 0 15.25 L 27.66 4.89 L 40.72 0 L 27.66 41.47 Z" fill="rgb(0, 46, 71)" height="41.47px" id="bO0KGNbMP" width="40.72px"/></g><path d="M 0 10.36 L 17.2 10.36 L 27.66 10.37 L 27.66 0 Z" fill="rgb(255, 157, 40)" height="10.369999999999948px" id="yxWIhUFzc" transform="translate(4.5 14.5)" width="27.659999999999997px"/><path d="M 0 4.89 L 0 41.48 L 13.06 0 Z" fill="rgb(105, 195, 234)" height="41.480000000000004px" id="xg4sf7mYx" transform="translate(32.5 9.5)" width="13.060000000000002px"/><path d="M 10.46 0.01 L 0 0 L 10.46 26.23 Z" fill="rgb(0, 79, 128)" height="26.229999999999993px" id="lwApAjh7Y" transform="translate(22 25)" width="10.460000000000008px"/><path d="M 0 0 L 19.88 6.73 L 17.2 0 Z" fill="rgb(225, 71, 72)" height="6.729999999999993px" id="K133X2hqC" transform="translate(4.5 25)" width="19.879999999999995px"/><path d="M 18.85 24.42 C 18.7 24.57 18.45 24.76 18.09 24.99 C 17.74 25.22 17.28 25.44 16.71 25.67 C 16.14 25.9 15.45 26.09 14.63 26.26 C 13.81 26.42 12.87 26.51 11.81 26.51 C 9.76 26.51 8 26.18 6.51 25.53 C 5.02 24.87 3.79 23.96 2.82 22.78 C 1.85 21.61 1.13 20.22 0.68 18.61 C 0.23 17.01 0 15.24 0 13.32 C 0 11.4 0.25 9.63 0.74 8 C 1.23 6.37 1.97 4.96 2.96 3.78 C 3.95 2.59 5.18 1.66 6.65 1 C 8.13 0.33 9.86 0 11.86 0 C 12.85 0 13.74 0.09 14.53 0.27 C 15.33 0.45 16.02 0.66 16.61 0.9 C 17.2 1.14 17.7 1.39 18.09 1.66 C 18.48 1.93 18.78 2.15 18.98 2.32 C 19.21 2.52 19.4 2.76 19.57 3.04 C 19.73 3.32 19.82 3.62 19.82 3.95 C 19.82 4.46 19.63 4.96 19.25 5.47 C 18.87 5.98 18.45 6.44 18 6.87 C 17.7 6.57 17.36 6.26 16.98 5.94 C 16.6 5.62 16.18 5.35 15.71 5.11 C 15.24 4.87 14.71 4.67 14.12 4.5 C 13.53 4.34 12.86 4.25 12.13 4.25 C 10.84 4.25 9.76 4.51 8.89 5.03 C 8.02 5.55 7.32 6.22 6.79 7.06 C 6.26 7.89 5.88 8.85 5.65 9.92 C 5.42 10.99 5.31 12.09 5.31 13.2 C 5.31 14.39 5.42 15.52 5.65 16.61 C 5.88 17.7 6.27 18.66 6.82 19.49 C 7.38 20.32 8.1 20.99 9 21.5 C 9.9 22.01 11.01 22.26 12.35 22.26 C 13.06 22.26 13.71 22.17 14.3 21.99 C 14.89 21.81 15.42 21.6 15.87 21.35 C 16.32 21.1 16.72 20.83 17.06 20.55 C 17.4 20.27 17.69 20.03 17.91 19.83 C 18.06 20.01 18.24 20.22 18.44 20.47 C 18.64 20.72 18.83 20.99 19.01 21.27 C 19.19 21.55 19.34 21.83 19.46 22.1 C 19.59 22.38 19.65 22.63 19.65 22.86 C 19.65 23.19 19.59 23.47 19.46 23.69 C 19.33 23.89 19.13 24.14 18.85 24.42 Z M 38.38 21.51 C 38.38 23.52 38.67 24.98 39.26 25.89 C 38.8 26.07 38.38 26.19 37.98 26.27 C 37.59 26.35 37.17 26.38 36.74 26.38 C 35.83 26.38 35.13 26.2 34.66 25.85 C 34.19 25.49 33.89 24.99 33.76 24.33 C 33.2 24.92 32.46 25.41 31.55 25.82 C 30.64 26.23 29.52 26.43 28.2 26.43 C 27.51 26.43 26.83 26.33 26.14 26.15 C 25.45 25.96 24.83 25.65 24.27 25.22 C 23.71 24.79 23.25 24.21 22.9 23.49 C 22.54 22.77 22.37 21.89 22.37 20.85 C 22.37 19.56 22.68 18.51 23.3 17.7 C 23.92 16.89 24.7 16.25 25.64 15.78 C 26.58 15.31 27.6 14.99 28.69 14.81 C 29.78 14.63 30.79 14.52 31.7 14.47 C 32.01 14.44 32.3 14.43 32.6 14.43 L 33.42 14.43 L 33.42 13.74 C 33.42 12.76 33.16 12.07 32.64 11.66 C 32.12 11.25 31.27 11.04 30.11 11.04 C 29.02 11.04 28.05 11.22 27.19 11.57 C 26.34 11.93 25.51 12.33 24.69 12.79 C 24.33 12.36 24.05 11.88 23.83 11.36 C 23.61 10.84 23.51 10.45 23.51 10.2 C 23.51 9.84 23.71 9.5 24.1 9.17 C 24.49 8.84 25.03 8.54 25.72 8.27 C 26.41 8 27.19 7.79 28.08 7.62 C 28.97 7.45 29.91 7.37 30.9 7.37 C 32.27 7.37 33.43 7.51 34.39 7.79 C 35.34 8.07 36.12 8.5 36.72 9.09 C 37.32 9.67 37.74 10.4 38 11.28 C 38.25 12.16 38.38 13.18 38.38 14.35 Z M 33.5 17.09 L 32.97 17.09 C 32.79 17.09 32.61 17.1 32.44 17.13 C 31.8 17.18 31.18 17.26 30.55 17.36 C 29.93 17.46 29.37 17.64 28.89 17.89 C 28.41 18.14 28.01 18.47 27.71 18.88 C 27.4 19.29 27.25 19.81 27.25 20.44 C 27.25 21.15 27.45 21.75 27.86 22.25 C 28.27 22.75 28.95 22.99 29.92 22.99 C 30.4 22.99 30.86 22.93 31.29 22.8 C 31.72 22.67 32.1 22.51 32.43 22.3 C 32.76 22.1 33.02 21.87 33.21 21.63 C 33.4 21.39 33.5 21.17 33.5 20.96 Z M 47.87 9.58 C 48.27 9.1 48.91 8.61 49.77 8.11 C 50.63 7.61 51.72 7.37 53.04 7.37 C 53.98 7.37 54.87 7.53 55.72 7.85 C 56.57 8.17 57.32 8.68 57.98 9.39 C 58.64 10.1 59.16 11.04 59.56 12.21 C 59.95 13.38 60.15 14.81 60.15 16.52 C 60.15 18.5 59.92 20.13 59.47 21.42 C 59.01 22.7 58.43 23.72 57.7 24.47 C 56.98 25.22 56.17 25.75 55.29 26.05 C 54.4 26.35 53.52 26.51 52.63 26.51 C 51.9 26.51 51.26 26.43 50.71 26.26 C 50.17 26.09 49.7 25.91 49.32 25.71 C 48.94 25.51 48.65 25.3 48.45 25.1 C 48.25 24.9 48.12 24.76 48.07 24.68 L 48.07 34.05 L 42.89 34.05 L 42.89 7.9 C 43.02 7.88 43.17 7.85 43.35 7.82 C 43.5 7.8 43.68 7.78 43.89 7.76 C 44.09 7.75 44.34 7.74 44.62 7.74 C 45.46 7.74 46.18 7.88 46.77 8.16 C 47.34 8.45 47.71 8.92 47.87 9.58 Z M 54.73 16.63 C 54.73 15.87 54.67 15.16 54.54 14.5 C 54.41 13.84 54.21 13.27 53.91 12.78 C 53.62 12.3 53.23 11.92 52.73 11.66 C 52.24 11.39 51.64 11.26 50.93 11.26 C 49.87 11.26 49.13 11.46 48.71 11.87 C 48.29 12.28 48.08 12.72 48.08 13.2 L 48.08 21.28 C 48.28 21.48 48.64 21.72 49.16 22 C 49.68 22.28 50.28 22.42 50.96 22.42 C 52.25 22.42 53.2 21.91 53.8 20.9 C 54.43 19.88 54.73 18.46 54.73 16.63 Z M 64.14 23.19 C 63.96 22.68 63.85 22.15 63.8 21.59 C 63.75 21.03 63.72 20.47 63.72 19.91 L 63.72 2.22 C 63.9 2.2 64.09 2.17 64.29 2.14 C 64.47 2.12 64.66 2.1 64.86 2.08 C 65.06 2.07 65.27 2.06 65.47 2.06 C 65.88 2.06 66.28 2.1 66.69 2.17 C 67.1 2.25 67.46 2.4 67.8 2.63 C 68.13 2.86 68.4 3.17 68.6 3.56 C 68.8 3.95 68.9 4.47 68.9 5.1 L 68.9 7.81 L 74.24 7.81 L 74.24 11.66 L 68.9 11.66 L 68.9 19.79 C 68.9 21.56 69.62 22.45 71.07 22.45 C 71.43 22.45 71.76 22.39 72.08 22.28 C 72.4 22.17 72.68 22.04 72.94 21.9 C 73.19 21.76 73.42 21.61 73.61 21.46 C 73.8 21.31 73.93 21.19 74.01 21.12 C 74.39 21.68 74.68 22.16 74.89 22.57 C 75.09 22.98 75.19 23.36 75.19 23.72 C 75.19 24.05 75.06 24.38 74.79 24.7 C 74.52 25.02 74.15 25.32 73.67 25.58 C 73.19 25.85 72.6 26.07 71.92 26.23 C 71.183 26.404 70.427 26.488 69.67 26.48 C 68.09 26.48 66.87 26.17 65.99 25.57 C 65.131 24.999 64.481 24.164 64.14 23.19 Z M 87.37 22.69 C 88.01 22.69 88.57 22.62 89.05 22.48 C 89.53 22.34 89.97 22.17 90.35 21.97 C 90.73 21.77 91.06 21.54 91.34 21.3 C 91.62 21.06 91.88 20.84 92.11 20.63 C 92.42 21.01 92.73 21.5 93.07 22.1 C 93.4 22.7 93.57 23.19 93.57 23.57 C 93.57 24.13 93.25 24.64 92.62 25.09 C 92.09 25.5 91.33 25.85 90.35 26.14 C 89.37 26.43 88.22 26.58 86.9 26.58 C 85.71 26.58 84.53 26.43 83.37 26.12 C 82.21 25.82 81.18 25.28 80.28 24.52 C 79.38 23.76 78.65 22.74 78.09 21.45 C 77.53 20.17 77.25 18.55 77.25 16.59 C 77.25 14.99 77.5 13.61 77.99 12.45 C 78.49 11.29 79.15 10.33 79.97 9.57 C 80.8 8.81 81.73 8.25 82.77 7.89 C 83.81 7.53 84.88 7.36 85.97 7.36 C 87.39 7.36 88.6 7.58 89.59 8.03 C 90.58 8.47 91.39 9.07 92.01 9.82 C 92.63 10.57 93.08 11.43 93.36 12.39 C 93.64 13.36 93.78 14.37 93.78 15.44 L 93.78 15.97 C 93.78 16.17 93.77 16.39 93.76 16.62 C 93.75 16.85 93.73 17.07 93.72 17.29 C 93.71 17.51 93.69 17.68 93.66 17.8 L 82.42 17.8 C 82.52 19.2 82.96 20.36 83.72 21.29 C 84.5 22.23 85.71 22.69 87.37 22.69 Z M 89.11 14.95 C 89.11 13.73 88.87 12.74 88.4 11.98 C 87.93 11.22 87.08 10.84 85.85 10.84 C 84.8 10.84 83.96 11.2 83.34 11.93 C 82.71 12.65 82.4 13.66 82.4 14.96 L 89.11 14.96 Z M 102.82 9.68 C 102.97 9.45 103.18 9.2 103.43 8.92 C 103.68 8.64 104 8.39 104.36 8.16 C 104.73 7.93 105.13 7.74 105.58 7.59 C 106.02 7.44 106.5 7.36 107.01 7.36 C 107.31 7.36 107.64 7.39 107.98 7.44 C 108.32 7.49 108.64 7.59 108.93 7.72 C 109.22 7.86 109.46 8.05 109.64 8.29 C 109.82 8.53 109.91 8.83 109.91 9.18 C 109.91 9.73 109.77 10.37 109.49 11.09 C 109.21 11.81 108.93 12.42 108.65 12.93 C 108.259 12.595 107.821 12.319 107.35 12.11 C 106.92 11.92 106.41 11.82 105.83 11.82 C 105.04 11.82 104.38 12.05 103.85 12.51 C 103.32 12.97 103.05 13.52 103.05 14.15 L 103.05 26.49 L 97.87 26.49 L 97.87 7.89 C 98 7.87 98.15 7.84 98.33 7.81 C 98.48 7.79 98.66 7.77 98.86 7.75 C 99.06 7.74 99.3 7.73 99.58 7.73 C 100.39 7.73 101.1 7.89 101.7 8.2 C 102.29 8.54 102.66 9.02 102.82 9.68 Z M 117.55 9.68 C 117.7 9.45 117.91 9.2 118.16 8.92 C 118.41 8.64 118.73 8.39 119.09 8.16 C 119.46 7.93 119.86 7.74 120.31 7.59 C 120.75 7.44 121.23 7.36 121.74 7.36 C 122.04 7.36 122.37 7.39 122.71 7.44 C 123.05 7.49 123.37 7.59 123.66 7.72 C 123.95 7.86 124.19 8.05 124.37 8.29 C 124.55 8.53 124.64 8.83 124.64 9.18 C 124.64 9.73 124.5 10.37 124.22 11.09 C 123.94 11.81 123.66 12.42 123.38 12.93 C 122.989 12.595 122.551 12.319 122.08 12.11 C 121.65 11.92 121.14 11.82 120.56 11.82 C 119.77 11.82 119.11 12.05 118.58 12.51 C 118.05 12.97 117.78 13.52 117.78 14.15 L 117.78 26.49 L 112.6 26.49 L 112.6 7.89 C 112.73 7.87 112.88 7.84 113.06 7.81 C 113.21 7.79 113.39 7.77 113.59 7.75 C 113.79 7.74 114.03 7.73 114.31 7.73 C 115.12 7.73 115.83 7.89 116.43 8.2 C 117.03 8.54 117.4 9.02 117.55 9.68 Z M 142.29 21.51 C 142.29 23.52 142.58 24.98 143.17 25.89 C 142.71 26.07 142.29 26.19 141.89 26.27 C 141.5 26.35 141.08 26.38 140.65 26.38 C 139.73 26.38 139.04 26.2 138.57 25.85 C 138.1 25.49 137.8 24.99 137.67 24.33 C 137.11 24.92 136.37 25.41 135.46 25.82 C 134.55 26.23 133.43 26.43 132.11 26.43 C 131.42 26.43 130.74 26.33 130.05 26.15 C 129.36 25.96 128.74 25.65 128.18 25.22 C 127.62 24.79 127.16 24.21 126.81 23.49 C 126.45 22.77 126.28 21.89 126.28 20.85 C 126.28 19.56 126.59 18.51 127.21 17.7 C 127.83 16.89 128.61 16.25 129.55 15.78 C 130.49 15.31 131.51 14.99 132.6 14.81 C 133.69 14.63 134.7 14.52 135.61 14.47 C 135.92 14.44 136.21 14.43 136.51 14.43 L 137.33 14.43 L 137.33 13.74 C 137.33 12.76 137.07 12.07 136.55 11.66 C 136.03 11.25 135.18 11.04 134.02 11.04 C 132.93 11.04 131.96 11.22 131.1 11.57 C 130.25 11.93 129.42 12.33 128.6 12.79 C 128.24 12.36 127.96 11.88 127.74 11.36 C 127.52 10.84 127.42 10.45 127.42 10.2 C 127.42 9.84 127.62 9.5 128.01 9.17 C 128.4 8.84 128.94 8.54 129.63 8.27 C 130.32 8 131.1 7.79 131.99 7.62 C 132.88 7.45 133.82 7.37 134.81 7.37 C 136.18 7.37 137.34 7.51 138.3 7.79 C 139.25 8.07 140.03 8.5 140.62 9.09 C 141.22 9.67 141.64 10.4 141.9 11.28 C 142.15 12.16 142.28 13.18 142.28 14.35 L 142.28 21.51 Z M 137.41 17.09 L 136.88 17.09 C 136.7 17.09 136.52 17.1 136.35 17.13 C 135.71 17.18 135.09 17.26 134.46 17.36 C 133.84 17.46 133.28 17.64 132.8 17.89 C 132.32 18.14 131.92 18.47 131.62 18.88 C 131.32 19.29 131.16 19.81 131.16 20.44 C 131.16 21.15 131.36 21.75 131.77 22.25 C 132.18 22.75 132.86 22.99 133.83 22.99 C 134.31 22.99 134.77 22.93 135.2 22.8 C 135.63 22.67 136.01 22.51 136.34 22.3 C 136.67 22.1 136.93 21.87 137.12 21.63 C 137.31 21.39 137.41 21.17 137.41 20.96 Z" fill="rgb(255, 255, 255)" height="34.049999885559075px" id="a3Cp4ysi6" transform="translate(49 17)" width="143.16999877929692px"/><g d="M 115.28 19.59 C 114.93 19.59 114.6 19.51 114.28 19.34 L 111 17.62 C 110.84 17.53 110.65 17.49 110.47 17.49 C 110.29 17.49 110.1 17.54 109.94 17.62 L 106.66 19.34 C 106.34 19.51 106.01 19.59 105.66 19.59 C 105.03 19.59 104.43 19.31 104.01 18.82 C 103.6 18.33 103.43 17.71 103.54 17.08 L 104.16 13.43 C 104.22 13.06 104.1 12.68 103.83 12.42 L 101.18 9.84 C 100.59 9.27 100.38 8.42 100.64 7.64 C 100.89 6.86 101.56 6.3 102.37 6.18 L 106.03 5.65 C 106.4 5.6 106.73 5.36 106.89 5.02 L 108.53 1.7 C 108.89 0.96 109.63 0.5 110.45 0.5 C 111.27 0.5 112.01 0.96 112.37 1.7 L 114.01 5.02 C 114.18 5.36 114.5 5.59 114.87 5.65 L 118.53 6.18 C 119.34 6.3 120.01 6.86 120.26 7.64 C 120.51 8.42 120.31 9.27 119.72 9.84 L 117.07 12.42 C 116.8 12.68 116.68 13.06 116.74 13.43 L 117.36 17.08 C 117.47 17.72 117.3 18.33 116.89 18.82 C 116.52 19.31 115.92 19.59 115.28 19.59 Z M 110.48 1 C 111.07 1 111.65 1.31 111.96 1.92 L 113.6 5.24 C 113.84 5.73 114.3 6.06 114.84 6.14 L 118.5 6.67 C 119.85 6.87 120.39 8.53 119.41 9.48 L 116.76 12.06 C 116.37 12.44 116.2 12.98 116.29 13.52 L 116.92 17.17 C 117.1 18.23 116.26 19.1 115.3 19.1 C 115.05 19.1 114.79 19.04 114.53 18.91 L 111.26 17.19 C 111.02 17.06 110.76 17 110.49 17 C 110.23 17 109.96 17.06 109.72 17.19 L 106.45 18.91 C 105.895 19.202 105.222 19.153 104.714 18.783 C 104.207 18.414 103.953 17.788 104.06 17.17 L 104.69 13.52 C 104.78 12.99 104.6 12.44 104.22 12.06 L 101.57 9.48 C 100.59 8.53 101.13 6.87 102.48 6.67 L 106.14 6.14 C 106.68 6.06 107.14 5.73 107.38 5.24 L 109.02 1.92 C 109.3 1.31 109.89 1 110.48 1 M 110.48 0 C 109.47 0 108.56 0.57 108.11 1.47 L 106.47 4.79 C 106.38 4.98 106.19 5.11 105.98 5.14 L 102.32 5.67 C 101.32 5.82 100.5 6.51 100.18 7.47 C 99.87 8.43 100.12 9.47 100.85 10.18 L 103.5 12.76 C 103.65 12.91 103.72 13.12 103.69 13.33 L 103.06 16.98 C 102.93 17.75 103.14 18.53 103.64 19.13 C 104.15 19.73 104.89 20.08 105.67 20.08 C 106.1 20.08 106.51 19.98 106.9 19.77 L 110.17 18.05 C 110.26 18 110.37 17.98 110.47 17.98 C 110.57 17.98 110.68 18.01 110.77 18.05 L 114.04 19.77 C 114.43 19.97 114.84 20.08 115.27 20.08 C 116.05 20.08 116.79 19.73 117.3 19.13 C 117.8 18.54 118.01 17.75 117.88 16.98 L 117.25 13.33 C 117.21 13.12 117.28 12.91 117.44 12.76 L 120.09 10.18 C 120.82 9.47 121.07 8.43 120.76 7.47 C 120.45 6.51 119.63 5.81 118.62 5.67 L 114.96 5.14 C 114.75 5.109 114.568 4.979 114.47 4.79 L 112.83 1.47 C 112.4 0.57 111.49 0 110.48 0 Z M 90.27 19.59 C 89.92 19.59 89.59 19.51 89.27 19.34 L 86 17.62 C 85.84 17.53 85.65 17.49 85.47 17.49 C 85.28 17.49 85.1 17.54 84.94 17.62 L 81.66 19.34 C 81.34 19.51 81.01 19.59 80.66 19.59 C 80.03 19.59 79.43 19.31 79.01 18.82 C 78.6 18.33 78.43 17.72 78.54 17.08 L 79.16 13.43 C 79.22 13.06 79.1 12.68 78.83 12.42 L 76.18 9.84 C 75.59 9.27 75.38 8.42 75.64 7.64 C 75.89 6.86 76.56 6.3 77.37 6.18 L 81.03 5.65 C 81.4 5.6 81.73 5.36 81.89 5.02 L 83.53 1.7 C 83.89 0.96 84.63 0.5 85.45 0.5 C 86.27 0.5 87.01 0.96 87.37 1.7 L 89.01 5.02 C 89.18 5.36 89.5 5.59 89.87 5.65 L 93.53 6.18 C 94.34 6.3 95.01 6.86 95.26 7.64 C 95.51 8.42 95.31 9.27 94.72 9.84 L 92.07 12.42 C 91.8 12.68 91.68 13.06 91.74 13.43 L 92.37 17.08 C 92.48 17.72 92.31 18.33 91.9 18.82 C 91.51 19.31 90.91 19.59 90.27 19.59 Z M 85.47 1 C 86.06 1 86.64 1.31 86.95 1.92 L 88.59 5.24 C 88.83 5.73 89.29 6.06 89.83 6.14 L 93.49 6.67 C 94.84 6.87 95.38 8.53 94.4 9.48 L 91.75 12.06 C 91.36 12.44 91.19 12.98 91.28 13.52 L 91.91 17.17 C 92.09 18.23 91.25 19.1 90.29 19.1 C 90.04 19.1 89.78 19.04 89.52 18.91 L 86.25 17.19 C 86.01 17.06 85.75 17 85.48 17 C 85.22 17 84.95 17.06 84.71 17.19 L 81.44 18.91 C 80.885 19.202 80.212 19.153 79.704 18.783 C 79.197 18.414 78.943 17.788 79.05 17.17 L 79.68 13.52 C 79.77 12.99 79.59 12.44 79.21 12.06 L 76.56 9.48 C 75.58 8.53 76.12 6.87 77.47 6.67 L 81.13 6.14 C 81.67 6.06 82.13 5.73 82.37 5.24 L 84.01 1.92 C 84.29 1.31 84.88 1 85.47 1 M 85.47 0 C 84.46 0 83.55 0.57 83.1 1.48 L 81.46 4.8 C 81.37 4.99 81.18 5.12 80.97 5.15 L 77.31 5.68 C 76.31 5.83 75.49 6.52 75.17 7.48 C 74.86 8.44 75.11 9.48 75.84 10.19 L 78.49 12.77 C 78.64 12.92 78.71 13.13 78.68 13.34 L 78.05 16.99 C 77.92 17.76 78.13 18.54 78.63 19.14 C 79.14 19.74 79.88 20.09 80.66 20.09 C 81.09 20.09 81.5 19.99 81.89 19.78 L 85.16 18.06 C 85.25 18.01 85.36 17.99 85.46 17.99 C 85.56 17.99 85.67 18.02 85.76 18.06 L 89.03 19.78 C 89.42 19.98 89.83 20.09 90.26 20.09 C 91.04 20.09 91.78 19.74 92.29 19.14 C 92.79 18.55 93 17.76 92.87 16.99 L 92.25 13.34 C 92.21 13.13 92.28 12.92 92.44 12.77 L 95.09 10.19 C 95.82 9.48 96.07 8.44 95.76 7.48 C 95.45 6.52 94.63 5.83 93.62 5.68 L 89.96 5.15 C 89.75 5.119 89.568 4.989 89.47 4.8 L 87.83 1.48 C 87.395 0.573 86.477 -0.003 85.47 0 Z M 65.26 19.59 C 64.91 19.59 64.58 19.51 64.26 19.34 L 60.99 17.62 C 60.83 17.53 60.64 17.49 60.46 17.49 C 60.27 17.49 60.09 17.54 59.93 17.62 L 56.65 19.34 C 56.33 19.51 56 19.59 55.65 19.59 C 55.02 19.59 54.42 19.31 54 18.82 C 53.59 18.33 53.42 17.72 53.53 17.08 L 54.16 13.43 C 54.22 13.06 54.1 12.68 53.83 12.42 L 51.18 9.84 C 50.59 9.27 50.38 8.42 50.64 7.64 C 50.89 6.86 51.56 6.3 52.37 6.18 L 56.03 5.65 C 56.4 5.6 56.73 5.36 56.89 5.02 L 58.53 1.7 C 58.89 0.96 59.63 0.5 60.45 0.5 C 61.27 0.5 62.01 0.96 62.37 1.7 L 64.01 5.02 C 64.18 5.36 64.5 5.59 64.87 5.65 L 68.53 6.18 C 69.34 6.3 70.01 6.86 70.26 7.64 C 70.51 8.42 70.31 9.27 69.72 9.84 L 67.07 12.42 C 66.8 12.68 66.68 13.06 66.74 13.43 L 67.36 17.08 C 67.47 17.72 67.3 18.33 66.89 18.82 C 66.49 19.31 65.89 19.59 65.26 19.59 Z M 60.45 1 C 61.04 1 61.62 1.31 61.93 1.92 L 63.57 5.24 C 63.81 5.73 64.27 6.06 64.81 6.14 L 68.47 6.67 C 69.82 6.87 70.36 8.53 69.38 9.48 L 66.73 12.06 C 66.34 12.44 66.17 12.98 66.26 13.52 L 66.89 17.17 C 67.07 18.23 66.23 19.1 65.27 19.1 C 65.02 19.1 64.76 19.04 64.5 18.91 L 61.23 17.19 C 60.99 17.06 60.73 17 60.46 17 C 60.2 17 59.93 17.06 59.69 17.19 L 56.42 18.91 C 55.865 19.202 55.192 19.153 54.684 18.783 C 54.177 18.414 53.923 17.788 54.03 17.17 L 54.66 13.52 C 54.75 12.99 54.57 12.44 54.19 12.06 L 51.54 9.48 C 50.56 8.53 51.1 6.87 52.45 6.67 L 56.11 6.14 C 56.65 6.06 57.11 5.73 57.35 5.24 L 58.99 1.92 C 59.28 1.31 59.87 1 60.45 1 M 60.45 0 C 59.44 0 58.53 0.57 58.08 1.48 L 56.44 4.8 C 56.35 4.99 56.16 5.12 55.95 5.15 L 52.29 5.68 C 51.29 5.83 50.47 6.52 50.15 7.48 C 49.84 8.44 50.09 9.48 50.82 10.19 L 53.47 12.77 C 53.62 12.92 53.69 13.13 53.66 13.34 L 53.03 16.99 C 52.9 17.76 53.11 18.54 53.61 19.14 C 54.12 19.74 54.86 20.09 55.64 20.09 C 56.07 20.09 56.48 19.99 56.87 19.78 L 60.14 18.06 C 60.23 18.01 60.34 17.99 60.44 17.99 C 60.54 17.99 60.65 18.02 60.74 18.06 L 64.01 19.78 C 64.4 19.98 64.81 20.09 65.24 20.09 C 66.02 20.09 66.76 19.74 67.27 19.14 C 67.77 18.55 67.98 17.76 67.85 16.99 L 67.22 13.34 C 67.18 13.13 67.25 12.92 67.41 12.77 L 70.06 10.19 C 70.79 9.48 71.04 8.44 70.73 7.48 C 70.42 6.52 69.6 5.82 68.59 5.68 L 64.93 5.15 C 64.72 5.119 64.538 4.989 64.44 4.8 L 62.8 1.48 C 62.38 0.57 61.47 0 60.45 0 Z M 40.25 19.59 C 39.9 19.59 39.57 19.51 39.25 19.34 L 35.97 17.62 C 35.81 17.53 35.62 17.49 35.44 17.49 C 35.26 17.49 35.07 17.54 34.91 17.62 L 31.63 19.34 C 31.31 19.51 30.98 19.59 30.63 19.59 C 30 19.59 29.4 19.31 28.98 18.82 C 28.57 18.33 28.4 17.71 28.51 17.08 L 29.13 13.43 C 29.19 13.06 29.07 12.68 28.8 12.42 L 26.15 9.84 C 25.56 9.27 25.35 8.42 25.61 7.64 C 25.86 6.86 26.53 6.3 27.34 6.18 L 31 5.65 C 31.37 5.6 31.7 5.36 31.86 5.02 L 33.5 1.7 C 33.86 0.96 34.6 0.5 35.42 0.5 C 36.24 0.5 36.98 0.96 37.34 1.7 L 38.98 5.02 C 39.15 5.36 39.47 5.59 39.84 5.65 L 43.5 6.18 C 44.31 6.3 44.98 6.86 45.23 7.64 C 45.48 8.42 45.28 9.27 44.69 9.84 L 42.04 12.42 C 41.77 12.68 41.65 13.06 41.71 13.43 L 42.33 17.08 C 42.44 17.72 42.27 18.33 41.86 18.82 C 41.48 19.31 40.88 19.59 40.25 19.59 Z M 35.44 1 C 36.03 1 36.61 1.31 36.92 1.92 L 38.56 5.24 C 38.8 5.73 39.26 6.06 39.8 6.14 L 43.46 6.67 C 44.81 6.87 45.35 8.53 44.37 9.48 L 41.72 12.06 C 41.33 12.44 41.16 12.98 41.25 13.52 L 41.88 17.17 C 42.06 18.23 41.22 19.1 40.26 19.1 C 40.01 19.1 39.75 19.04 39.49 18.91 L 36.22 17.19 C 35.98 17.06 35.72 17 35.45 17 C 35.19 17 34.92 17.06 34.68 17.19 L 31.41 18.91 C 30.855 19.202 30.182 19.153 29.674 18.783 C 29.167 18.414 28.913 17.788 29.02 17.17 L 29.65 13.52 C 29.74 12.99 29.56 12.44 29.18 12.06 L 26.53 9.48 C 25.55 8.53 26.09 6.87 27.44 6.67 L 31.1 6.14 C 31.64 6.06 32.1 5.73 32.34 5.24 L 33.98 1.92 C 34.27 1.31 34.86 1 35.44 1 M 35.44 0 C 34.43 0 33.52 0.57 33.07 1.47 L 31.43 4.79 C 31.34 4.98 31.15 5.11 30.94 5.14 L 27.28 5.67 C 26.28 5.82 25.46 6.51 25.14 7.47 C 24.82 8.43 25.08 9.47 25.81 10.18 L 28.46 12.76 C 28.61 12.91 28.68 13.12 28.65 13.33 L 28.03 16.99 C 27.9 17.76 28.11 18.54 28.61 19.14 C 29.12 19.74 29.86 20.09 30.64 20.09 C 31.07 20.09 31.48 19.99 31.87 19.78 L 35.14 18.06 C 35.23 18.01 35.34 17.99 35.44 17.99 C 35.54 17.99 35.65 18.02 35.74 18.06 L 39.01 19.78 C 39.4 19.98 39.81 20.09 40.24 20.09 C 41.02 20.09 41.76 19.74 42.27 19.14 C 42.77 18.55 42.98 17.76 42.85 16.99 L 42.22 13.34 C 42.18 13.13 42.25 12.92 42.41 12.77 L 45.06 10.19 C 45.79 9.48 46.04 8.44 45.73 7.48 C 45.42 6.52 44.6 5.82 43.59 5.68 L 39.93 5.15 C 39.72 5.119 39.538 4.989 39.44 4.8 L 37.8 1.48 C 37.369 0.57 36.448 -0.008 35.44 0 Z M 15.24 19.59 C 14.89 19.59 14.56 19.51 14.24 19.34 L 10.97 17.62 C 10.81 17.53 10.62 17.49 10.44 17.49 C 10.26 17.49 10.07 17.54 9.91 17.62 L 6.63 19.34 C 6.31 19.51 5.98 19.59 5.63 19.59 C 5 19.59 4.4 19.31 3.98 18.82 C 3.57 18.33 3.4 17.71 3.51 17.08 L 4.13 13.43 C 4.19 13.06 4.07 12.68 3.8 12.42 L 1.15 9.84 C 0.56 9.27 0.35 8.42 0.61 7.64 C 0.86 6.86 1.53 6.3 2.34 6.18 L 6 5.65 C 6.37 5.6 6.7 5.36 6.86 5.02 L 8.5 1.7 C 8.86 0.96 9.6 0.5 10.42 0.5 C 11.24 0.5 11.98 0.96 12.34 1.7 L 13.98 5.02 C 14.15 5.36 14.47 5.59 14.84 5.65 L 18.5 6.18 C 19.31 6.3 19.98 6.86 20.23 7.64 C 20.48 8.42 20.28 9.27 19.69 9.84 L 17.04 12.42 C 16.77 12.68 16.65 13.06 16.71 13.43 L 17.34 17.08 C 17.45 17.72 17.28 18.33 16.87 18.82 C 16.47 19.31 15.87 19.59 15.24 19.59 Z M 10.43 1 C 11.02 1 11.6 1.31 11.91 1.92 L 13.55 5.24 C 13.79 5.73 14.25 6.06 14.79 6.14 L 18.45 6.67 C 19.8 6.87 20.34 8.53 19.36 9.48 L 16.71 12.06 C 16.32 12.44 16.15 12.98 16.24 13.52 L 16.87 17.17 C 17.05 18.23 16.21 19.1 15.25 19.1 C 15 19.1 14.74 19.04 14.48 18.91 L 11.21 17.19 C 10.97 17.06 10.71 17 10.44 17 C 10.18 17 9.91 17.06 9.67 17.19 L 6.4 18.91 C 5.845 19.202 5.172 19.153 4.664 18.783 C 4.157 18.414 3.903 17.788 4.01 17.17 L 4.64 13.52 C 4.73 12.99 4.55 12.44 4.17 12.06 L 1.52 9.48 C 0.54 8.53 1.08 6.87 2.43 6.67 L 6.09 6.14 C 6.63 6.06 7.09 5.73 7.33 5.24 L 8.97 1.92 C 9.26 1.31 9.84 1 10.43 1 M 10.43 0 C 9.42 0 8.51 0.57 8.06 1.48 L 6.42 4.8 C 6.33 4.99 6.14 5.12 5.93 5.15 L 2.27 5.68 C 1.27 5.83 0.45 6.52 0.13 7.48 C -0.18 8.44 0.07 9.48 0.8 10.19 L 3.45 12.77 C 3.6 12.92 3.67 13.13 3.64 13.34 L 3.01 16.99 C 2.88 17.76 3.09 18.54 3.59 19.14 C 4.1 19.74 4.84 20.09 5.62 20.09 C 6.05 20.09 6.46 19.99 6.85 19.78 L 10.12 18.06 C 10.21 18.01 10.32 17.99 10.42 17.99 C 10.52 17.99 10.63 18.02 10.72 18.06 L 13.99 19.78 C 14.38 19.98 14.79 20.09 15.22 20.09 C 16 20.09 16.74 19.74 17.25 19.14 C 17.75 18.55 17.96 17.76 17.83 16.99 L 17.21 13.34 C 17.17 13.13 17.24 12.92 17.4 12.77 L 20.05 10.19 C 20.78 9.48 21.03 8.44 20.72 7.48 C 20.41 6.52 19.59 5.83 18.58 5.68 L 14.92 5.15 C 14.71 5.119 14.528 4.989 14.43 4.8 L 12.79 1.48 C 12.355 0.573 11.437 -0.003 10.43 0 Z" fill="transparent" height="20.09008171389698px" id="bj36hCBvj" transform="translate(72.5 53.5)" width="120.89090557288256px"><path d="M 14.75 19.09 C 14.4 19.09 14.07 19.01 13.75 18.84 L 10.47 17.12 C 10.31 17.03 10.12 16.99 9.94 16.99 C 9.76 16.99 9.57 17.04 9.41 17.12 L 6.13 18.84 C 5.81 19.01 5.48 19.09 5.13 19.09 C 4.5 19.09 3.9 18.81 3.48 18.32 C 3.07 17.83 2.9 17.21 3.01 16.58 L 3.63 12.93 C 3.69 12.56 3.57 12.18 3.3 11.92 L 0.65 9.34 C 0.06 8.77 -0.15 7.92 0.11 7.14 C 0.36 6.36 1.03 5.8 1.84 5.68 L 5.5 5.15 C 5.87 5.1 6.2 4.86 6.36 4.52 L 8 1.2 C 8.36 0.46 9.1 0 9.92 0 C 10.74 0 11.48 0.46 11.84 1.2 L 13.48 4.52 C 13.65 4.86 13.97 5.09 14.34 5.15 L 18 5.68 C 18.81 5.8 19.48 6.36 19.73 7.14 C 19.98 7.92 19.78 8.77 19.19 9.34 L 16.54 11.92 C 16.27 12.18 16.15 12.56 16.21 12.93 L 16.83 16.58 C 16.94 17.22 16.77 17.83 16.36 18.32 C 15.99 18.81 15.39 19.09 14.75 19.09 Z" fill="rgb(255, 157, 40)" height="19.09000000000001px" id="IbFKePeI4" transform="translate(100.531 0.5)" width="19.835346538708947px"/><path d="M 34.95 1 C 35.54 1 36.12 1.31 36.43 1.92 L 38.07 5.24 C 38.31 5.73 38.77 6.06 39.31 6.14 L 42.97 6.67 C 44.32 6.87 44.86 8.53 43.88 9.48 L 41.23 12.06 C 40.84 12.44 40.67 12.98 40.76 13.52 L 41.39 17.17 C 41.57 18.23 40.73 19.1 39.77 19.1 C 39.52 19.1 39.26 19.04 39 18.91 L 35.73 17.19 C 35.49 17.06 35.23 17 34.96 17 C 34.7 17 34.43 17.06 34.19 17.19 L 30.92 18.91 C 30.364 19.202 29.691 19.153 29.184 18.783 C 28.676 18.414 28.423 17.788 28.53 17.17 L 29.16 13.52 C 29.25 12.99 29.07 12.44 28.69 12.06 L 26.04 9.48 C 25.06 8.53 25.6 6.87 26.95 6.67 L 30.61 6.14 C 31.15 6.06 31.61 5.73 31.85 5.24 L 33.49 1.92 C 33.77 1.31 34.36 1 34.95 1 M 34.95 0 C 33.94 0 33.03 0.57 32.58 1.47 L 30.94 4.79 C 30.85 4.98 30.66 5.11 30.45 5.14 L 26.79 5.67 C 25.79 5.82 24.97 6.51 24.65 7.47 C 24.34 8.43 24.59 9.47 25.32 10.18 L 27.97 12.76 C 28.12 12.91 28.19 13.12 28.16 13.33 L 27.53 16.98 C 27.4 17.75 27.61 18.53 28.11 19.13 C 28.62 19.73 29.36 20.08 30.14 20.08 C 30.57 20.08 30.98 19.98 31.37 19.77 L 34.64 18.05 C 34.73 18 34.84 17.98 34.94 17.98 C 35.04 17.98 35.15 18.01 35.24 18.05 L 38.51 19.77 C 38.9 19.97 39.31 20.08 39.74 20.08 C 40.52 20.08 41.26 19.73 41.77 19.13 C 42.27 18.54 42.48 17.75 42.35 16.98 L 41.72 13.33 C 41.68 13.12 41.75 12.91 41.91 12.76 L 44.56 10.18 C 45.29 9.47 45.54 8.43 45.23 7.47 C 44.92 6.51 44.1 5.81 43.09 5.67 L 39.43 5.14 C 39.22 5.109 39.037 4.979 38.94 4.79 L 37.3 1.47 C 36.87 0.57 35.96 0 34.95 0 Z M 14.74 19.59 C 14.39 19.59 14.06 19.51 13.74 19.34 L 10.47 17.62 C 10.31 17.53 10.12 17.49 9.94 17.49 C 9.75 17.49 9.57 17.54 9.41 17.62 L 6.13 19.34 C 5.81 19.51 5.48 19.59 5.13 19.59 C 4.5 19.59 3.9 19.31 3.48 18.82 C 3.07 18.33 2.9 17.72 3.01 17.08 L 3.63 13.43 C 3.69 13.06 3.57 12.68 3.3 12.42 L 0.65 9.84 C 0.06 9.27 -0.15 8.42 0.11 7.64 C 0.36 6.86 1.03 6.3 1.84 6.18 L 5.5 5.65 C 5.87 5.6 6.2 5.36 6.36 5.02 L 8 1.7 C 8.36 0.96 9.1 0.5 9.92 0.5 C 10.74 0.5 11.48 0.96 11.84 1.7 L 13.48 5.02 C 13.65 5.36 13.97 5.59 14.34 5.65 L 18 6.18 C 18.81 6.3 19.48 6.86 19.73 7.64 C 19.98 8.42 19.78 9.27 19.19 9.84 L 16.54 12.42 C 16.27 12.68 16.15 13.06 16.21 13.43 L 16.84 17.08 C 16.95 17.72 16.78 18.33 16.37 18.82 C 15.98 19.31 15.38 19.59 14.74 19.59 Z" fill="rgb(255, 157, 40)" height="20.08px" id="GrfCV8C6O" transform="translate(75.531 0)" width="45.36031170081223px"/><path d="M 34.94 1 C 35.53 1 36.11 1.31 36.42 1.92 L 38.06 5.24 C 38.3 5.73 38.76 6.06 39.3 6.14 L 42.96 6.67 C 44.31 6.87 44.85 8.53 43.87 9.48 L 41.22 12.06 C 40.83 12.44 40.66 12.98 40.75 13.52 L 41.38 17.17 C 41.56 18.23 40.72 19.1 39.76 19.1 C 39.51 19.1 39.25 19.04 38.99 18.91 L 35.72 17.19 C 35.48 17.06 35.22 17 34.95 17 C 34.69 17 34.42 17.06 34.18 17.19 L 30.91 18.91 C 30.354 19.202 29.681 19.153 29.174 18.783 C 28.666 18.414 28.413 17.788 28.52 17.17 L 29.15 13.52 C 29.24 12.99 29.06 12.44 28.68 12.06 L 26.03 9.48 C 25.05 8.53 25.59 6.87 26.94 6.67 L 30.6 6.14 C 31.14 6.06 31.6 5.73 31.84 5.24 L 33.48 1.92 C 33.76 1.31 34.35 1 34.94 1 M 34.94 0 C 33.93 0 33.02 0.57 32.57 1.48 L 30.93 4.8 C 30.84 4.99 30.65 5.12 30.44 5.15 L 26.78 5.68 C 25.78 5.83 24.96 6.52 24.64 7.48 C 24.33 8.44 24.58 9.48 25.31 10.19 L 27.96 12.77 C 28.11 12.92 28.18 13.13 28.15 13.34 L 27.52 16.99 C 27.39 17.76 27.6 18.54 28.1 19.14 C 28.61 19.74 29.35 20.09 30.13 20.09 C 30.56 20.09 30.97 19.99 31.36 19.78 L 34.63 18.06 C 34.72 18.01 34.83 17.99 34.93 17.99 C 35.03 17.99 35.14 18.02 35.23 18.06 L 38.5 19.78 C 38.89 19.98 39.3 20.09 39.73 20.09 C 40.51 20.09 41.25 19.74 41.76 19.14 C 42.26 18.55 42.47 17.76 42.34 16.99 L 41.72 13.34 C 41.68 13.13 41.75 12.92 41.91 12.77 L 44.56 10.19 C 45.29 9.48 45.54 8.44 45.23 7.48 C 44.92 6.52 44.1 5.83 43.09 5.68 L 39.43 5.15 C 39.22 5.119 39.037 4.989 38.94 4.8 L 37.3 1.48 C 36.864 0.573 35.946 -0.003 34.94 0 Z M 14.73 19.59 C 14.38 19.59 14.05 19.51 13.73 19.34 L 10.46 17.62 C 10.3 17.53 10.11 17.49 9.93 17.49 C 9.74 17.49 9.56 17.54 9.4 17.62 L 6.12 19.34 C 5.8 19.51 5.47 19.59 5.12 19.59 C 4.49 19.59 3.89 19.31 3.47 18.82 C 3.06 18.33 2.89 17.72 3 17.08 L 3.63 13.43 C 3.69 13.06 3.57 12.68 3.3 12.42 L 0.65 9.84 C 0.06 9.27 -0.15 8.42 0.11 7.64 C 0.36 6.86 1.03 6.3 1.84 6.18 L 5.5 5.65 C 5.87 5.6 6.2 5.36 6.36 5.02 L 8 1.7 C 8.36 0.96 9.1 0.5 9.92 0.5 C 10.74 0.5 11.48 0.96 11.84 1.7 L 13.48 5.02 C 13.65 5.36 13.97 5.59 14.34 5.65 L 18 6.18 C 18.81 6.3 19.48 6.86 19.73 7.64 C 19.98 8.42 19.78 9.27 19.19 9.84 L 16.54 12.42 C 16.27 12.68 16.15 13.06 16.21 13.43 L 16.83 17.08 C 16.94 17.72 16.77 18.33 16.36 18.82 C 15.96 19.31 15.36 19.59 14.73 19.59 Z" fill="rgb(255, 157, 40)" height="20.090010253703277px" id="DrjXCW3m9" transform="translate(50.531 0)" width="45.360311471930395px"/><path d="M 34.95 1 C 35.54 1 36.12 1.31 36.43 1.92 L 38.07 5.24 C 38.31 5.73 38.77 6.06 39.31 6.14 L 42.97 6.67 C 44.32 6.87 44.86 8.53 43.88 9.48 L 41.23 12.06 C 40.84 12.44 40.67 12.98 40.76 13.52 L 41.39 17.17 C 41.57 18.23 40.73 19.1 39.77 19.1 C 39.52 19.1 39.26 19.04 39 18.91 L 35.73 17.19 C 35.49 17.06 35.23 17 34.96 17 C 34.7 17 34.43 17.06 34.19 17.19 L 30.92 18.91 C 30.364 19.202 29.691 19.153 29.184 18.783 C 28.676 18.414 28.423 17.788 28.53 17.17 L 29.16 13.52 C 29.25 12.99 29.07 12.44 28.69 12.06 L 26.04 9.48 C 25.06 8.53 25.6 6.87 26.95 6.67 L 30.61 6.14 C 31.15 6.06 31.61 5.73 31.85 5.24 L 33.49 1.92 C 33.78 1.31 34.37 1 34.95 1 M 34.95 0 C 33.94 0 33.03 0.57 32.58 1.48 L 30.94 4.8 C 30.85 4.99 30.66 5.12 30.45 5.15 L 26.79 5.68 C 25.79 5.83 24.97 6.52 24.65 7.48 C 24.34 8.44 24.59 9.48 25.32 10.19 L 27.97 12.77 C 28.12 12.92 28.19 13.13 28.16 13.34 L 27.53 16.99 C 27.4 17.76 27.61 18.54 28.11 19.14 C 28.62 19.74 29.36 20.09 30.14 20.09 C 30.57 20.09 30.98 19.99 31.37 19.78 L 34.64 18.06 C 34.73 18.01 34.84 17.99 34.94 17.99 C 35.04 17.99 35.15 18.02 35.24 18.06 L 38.51 19.78 C 38.9 19.98 39.31 20.09 39.74 20.09 C 40.52 20.09 41.26 19.74 41.77 19.14 C 42.27 18.55 42.48 17.76 42.35 16.99 L 41.72 13.34 C 41.68 13.13 41.75 12.92 41.91 12.77 L 44.56 10.19 C 45.29 9.48 45.54 8.44 45.23 7.48 C 44.92 6.52 44.1 5.82 43.09 5.68 L 39.43 5.15 C 39.22 5.119 39.037 4.989 38.94 4.8 L 37.3 1.48 C 36.88 0.57 35.97 0 34.95 0 Z M 14.75 19.59 C 14.4 19.59 14.07 19.51 13.75 19.34 L 10.47 17.62 C 10.31 17.53 10.12 17.49 9.94 17.49 C 9.76 17.49 9.57 17.54 9.41 17.62 L 6.13 19.34 C 5.81 19.51 5.48 19.59 5.13 19.59 C 4.5 19.59 3.9 19.31 3.48 18.82 C 3.07 18.33 2.9 17.71 3.01 17.08 L 3.63 13.43 C 3.69 13.06 3.57 12.68 3.3 12.42 L 0.65 9.84 C 0.06 9.27 -0.15 8.42 0.11 7.64 C 0.36 6.86 1.03 6.3 1.84 6.18 L 5.5 5.65 C 5.87 5.6 6.2 5.36 6.36 5.02 L 8 1.7 C 8.36 0.96 9.1 0.5 9.92 0.5 C 10.74 0.5 11.48 0.96 11.84 1.7 L 13.48 5.02 C 13.65 5.36 13.97 5.59 14.34 5.65 L 18 6.18 C 18.81 6.3 19.48 6.86 19.73 7.64 C 19.98 8.42 19.78 9.27 19.19 9.84 L 16.54 12.42 C 16.27 12.68 16.15 13.06 16.21 13.43 L 16.83 17.08 C 16.94 17.72 16.77 18.33 16.36 18.82 C 15.98 19.31 15.38 19.59 14.75 19.59 Z" fill="rgb(255, 157, 40)" height="20.090000000000003px" id="ngoE9wyNC" transform="translate(25.501 0)" width="45.36031170081222px"/><path d="M 34.94 1 C 35.53 1 36.11 1.31 36.42 1.92 L 38.06 5.24 C 38.3 5.73 38.76 6.06 39.3 6.14 L 42.96 6.67 C 44.31 6.87 44.85 8.53 43.87 9.48 L 41.22 12.06 C 40.83 12.44 40.66 12.98 40.75 13.52 L 41.38 17.17 C 41.56 18.23 40.72 19.1 39.76 19.1 C 39.51 19.1 39.25 19.04 38.99 18.91 L 35.72 17.19 C 35.48 17.06 35.22 17 34.95 17 C 34.69 17 34.42 17.06 34.18 17.19 L 30.91 18.91 C 30.354 19.202 29.681 19.153 29.174 18.783 C 28.666 18.414 28.413 17.788 28.52 17.17 L 29.15 13.52 C 29.24 12.99 29.06 12.44 28.68 12.06 L 26.03 9.48 C 25.05 8.53 25.59 6.87 26.94 6.67 L 30.6 6.14 C 31.14 6.06 31.6 5.73 31.84 5.24 L 33.48 1.92 C 33.77 1.31 34.36 1 34.94 1 M 34.94 0 C 33.93 0 33.02 0.57 32.57 1.47 L 30.93 4.79 C 30.84 4.98 30.65 5.11 30.44 5.14 L 26.78 5.67 C 25.78 5.82 24.96 6.51 24.64 7.47 C 24.32 8.43 24.58 9.47 25.31 10.18 L 27.96 12.76 C 28.11 12.91 28.18 13.12 28.15 13.33 L 27.53 16.99 C 27.4 17.76 27.61 18.54 28.11 19.14 C 28.62 19.74 29.36 20.09 30.14 20.09 C 30.57 20.09 30.98 19.99 31.37 19.78 L 34.64 18.06 C 34.73 18.01 34.84 17.99 34.94 17.99 C 35.04 17.99 35.15 18.02 35.24 18.06 L 38.51 19.78 C 38.9 19.98 39.31 20.09 39.74 20.09 C 40.52 20.09 41.26 19.74 41.77 19.14 C 42.27 18.55 42.48 17.76 42.35 16.99 L 41.72 13.34 C 41.68 13.13 41.75 12.92 41.91 12.77 L 44.56 10.19 C 45.29 9.48 45.54 8.44 45.23 7.48 C 44.92 6.52 44.1 5.82 43.09 5.68 L 39.43 5.15 C 39.22 5.119 39.037 4.989 38.94 4.8 L 37.3 1.48 C 36.868 0.57 35.948 -0.008 34.94 0 Z M 14.74 19.59 C 14.39 19.59 14.06 19.51 13.74 19.34 L 10.47 17.62 C 10.31 17.53 10.12 17.49 9.94 17.49 C 9.76 17.49 9.57 17.54 9.41 17.62 L 6.13 19.34 C 5.81 19.51 5.48 19.59 5.13 19.59 C 4.5 19.59 3.9 19.31 3.48 18.82 C 3.07 18.33 2.9 17.71 3.01 17.08 L 3.63 13.43 C 3.69 13.06 3.57 12.68 3.3 12.42 L 0.65 9.84 C 0.06 9.27 -0.15 8.42 0.11 7.64 C 0.36 6.86 1.03 6.3 1.84 6.18 L 5.5 5.65 C 5.87 5.6 6.2 5.36 6.36 5.02 L 8 1.7 C 8.36 0.96 9.1 0.5 9.92 0.5 C 10.74 0.5 11.48 0.96 11.84 1.7 L 13.48 5.02 C 13.65 5.36 13.97 5.59 14.34 5.65 L 18 6.18 C 18.81 6.3 19.48 6.86 19.73 7.64 C 19.98 8.42 19.78 9.27 19.19 9.84 L 16.54 12.42 C 16.27 12.68 16.15 13.06 16.21 13.43 L 16.84 17.08 C 16.95 17.72 16.78 18.33 16.37 18.82 C 15.97 19.31 15.37 19.59 14.74 19.59 Z" fill="rgb(255, 157, 40)" height="20.09008171389698px" id="wrJ6ATfM2" transform="translate(0.501 0)" width="45.360310123436875px"/><path d="M 10.43 1 C 11.02 1 11.6 1.31 11.91 1.92 L 13.55 5.24 C 13.79 5.73 14.25 6.06 14.79 6.14 L 18.45 6.67 C 19.8 6.87 20.34 8.53 19.36 9.48 L 16.71 12.06 C 16.32 12.44 16.15 12.98 16.24 13.52 L 16.87 17.17 C 17.05 18.23 16.21 19.1 15.25 19.1 C 15 19.1 14.74 19.04 14.48 18.91 L 11.21 17.19 C 10.97 17.06 10.71 17 10.44 17 C 10.18 17 9.91 17.06 9.67 17.19 L 6.4 18.91 C 5.845 19.202 5.172 19.153 4.664 18.783 C 4.157 18.414 3.903 17.788 4.01 17.17 L 4.64 13.52 C 4.73 12.99 4.55 12.44 4.17 12.06 L 1.52 9.48 C 0.54 8.53 1.08 6.87 2.43 6.67 L 6.09 6.14 C 6.63 6.06 7.09 5.73 7.33 5.24 L 8.97 1.92 C 9.26 1.31 9.84 1 10.43 1 M 10.43 0 C 9.42 0 8.51 0.57 8.06 1.48 L 6.42 4.8 C 6.33 4.99 6.14 5.12 5.93 5.15 L 2.27 5.68 C 1.27 5.83 0.45 6.52 0.13 7.48 C -0.18 8.44 0.07 9.48 0.8 10.19 L 3.45 12.77 C 3.6 12.92 3.67 13.13 3.64 13.34 L 3.01 16.99 C 2.88 17.76 3.09 18.54 3.59 19.14 C 4.1 19.74 4.84 20.09 5.62 20.09 C 6.05 20.09 6.46 19.99 6.85 19.78 L 10.12 18.06 C 10.21 18.01 10.32 17.99 10.42 17.99 C 10.52 17.99 10.63 18.02 10.72 18.06 L 13.99 19.78 C 14.38 19.98 14.79 20.09 15.22 20.09 C 16 20.09 16.74 19.74 17.25 19.14 C 17.75 18.55 17.96 17.76 17.83 16.99 L 17.21 13.34 C 17.17 13.13 17.24 12.92 17.4 12.77 L 20.05 10.19 C 20.78 9.48 21.03 8.44 20.72 7.48 C 20.41 6.52 19.59 5.83 18.58 5.68 L 14.92 5.15 C 14.71 5.119 14.528 4.989 14.43 4.8 L 12.79 1.48 C 12.355 0.573 11.437 -0.003 10.43 0 Z" fill="rgb(255, 157, 40)" height="20.090010253703277px" id="hJFYe3dIa" transform="translate(0 0)" width="20.850908243170604px"/></g><path d="M 0 0 L 0 56.4" fill="transparent" height="56.400000000000006px" id="SUvQqLifm" stroke-dasharray="" stroke-linecap="round" stroke-linejoin="miter" stroke-miterlimit="10" stroke-width="0.408" stroke="rgb(104, 197, 237)" transform="translate(203 17)" width="1px"/></g></svg>)

VAT returns for translators: A complete guide

Do translators need to file VAT returns?

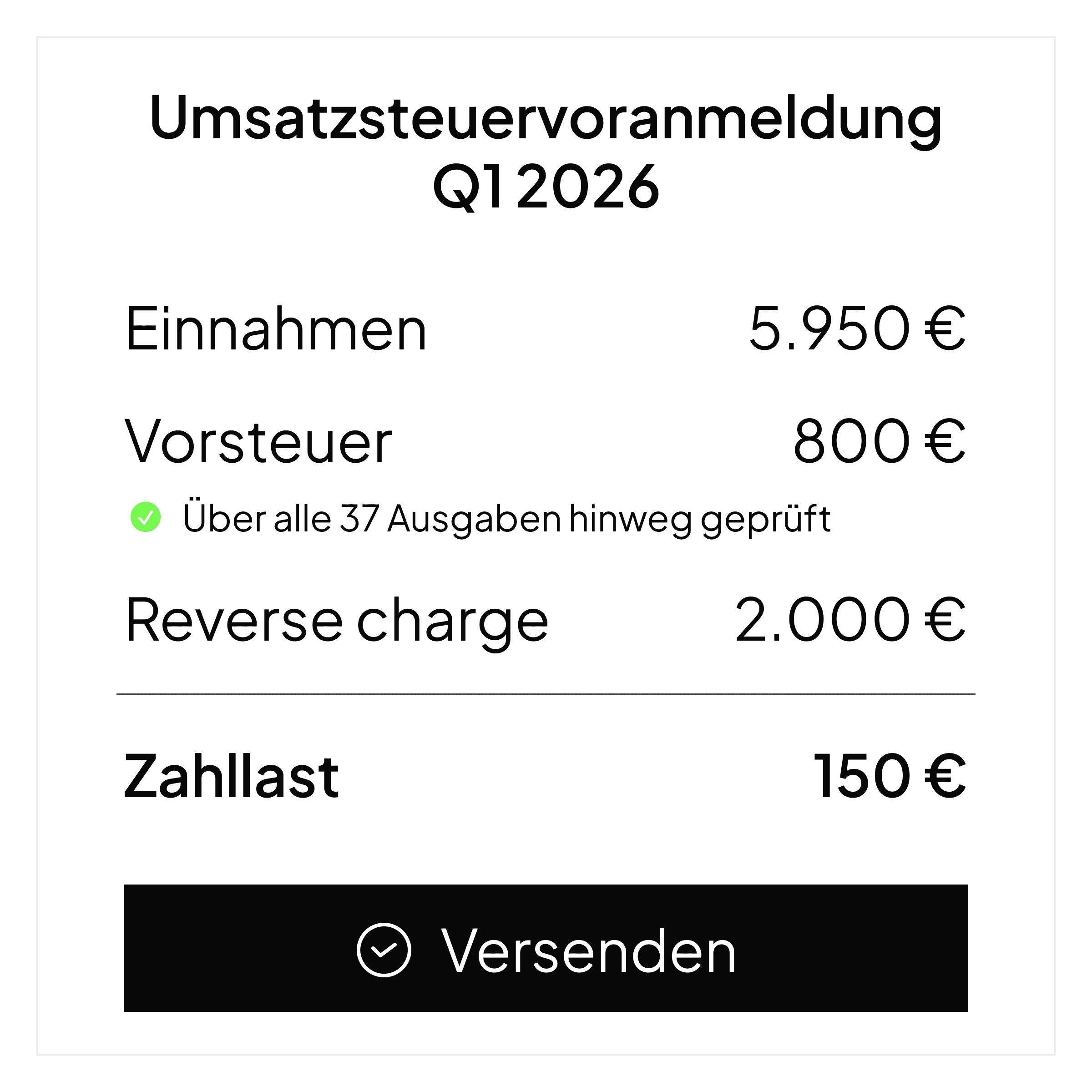

If you're a freelance translator in Germany earning above €25,000/year, you must register for VAT and file regular Umsatzsteuervoranmeldungen. This applies whether you translate legal documents, marketing materials, technical manuals, or literary works.

Understanding VAT for international clients

Translators often have a more international client base than other freelancers. VAT treatment differs based on where your client is located:

German clients: Charge 19% VAT.

EU business clients: Apply reverse charge (0% VAT, client self-accounts).

EU private consumers: Charge 19% VAT.

Non-EU clients: Usually 0% VAT (export of services).

Getting this right is crucial for correct UStVA filing.

What expenses can translators deduct?

Translation has modest but consistent business expenses:

CAT tools (SDL Trados, MemoQ, Wordfast),

Dictionaries and reference materials,

Terminology databases,

Professional memberships (BDÜ, etc.),

Training and certifications,

Home office expenses,

Computer and software.

Every VAT euro on these expenses can be reclaimed.

Common VAT mistakes translators make

Wrong VAT on international invoices: Charging 19% to a US company is incorrect. Not charging VAT to a French private consumer is also wrong.

Missing reverse charge declarations: EU B2B clients need proper reverse charge invoices with their VAT ID.

Ignoring platform fees: If you work through translation platforms, their fees usually include deductible VAT.

How Norman helps translators

Norman connects to your bank and automatically identifies client payments by location. It applies correct VAT treatment—19% for domestic, reverse charge for EU B2B, zero-rate for non-EU—and pre-fills your UStVA with accurate numbers.